April 2018 Newsletter

April Newsletter:

Patience + Transformational Change = 10X Outperformance

Dear Subscriber,

What we have here is your normal average bull market nervous breakdown. S&P 500 2580 is the “line in the sand.” We test it over and over and over again. It’s a bottom. Investor confidence is a funny thing; 4 months ago we had a bullish “Geosynchronous Expansion” for the first time 2010. Four months ago we had a ‘terrific corp tax cut” that will unleash $1 trillion of new marginal spending by corporations. 4 months ago we had no tariffs or

The Value of Patience: Transformational Sectors & IP Leaders+Patience + TR MacroMarket Index Timing = Extraordinary Profitsspectre of a trade war.

Confidence is being subsumed with the worries at the moment:

About a China trade war (and the murder’s row of U.S. populists and trade war folks now meeting with China)

What Mueller REALLY has on Trump (beyond the 3000+ fact-checked lies/incorrect and/or bogus statements/made up statements in general)

Strengthening Dollar

>3% bond yields

2% inflation (really?)

The Fed tightening too much in 2019

The geosynchronous economic expansion (All Euro nations with slightly lower PMI reports aka Growth Peak)

Higher borrowing costs for companies with LIBOR priced debt

Earnings vs. expectations as always

New global regulation of big cap Facebook/Google

Higher volatility: 16 VIX is a 1% move in the S&P--no whoop. The clean-out of the “Sell VIX premium” investors and rising short term rates DO INCREASE volatility to normal

The Death of FAANG (Facebook, Apple, Alphabet, Netflix, Amazon)

25% tariffs on semiconductors sold from the U.S. based companies to China

That’s a Baker’s Dozen of worries YET we are UP @11% for the year (thank you Micron and other hedges + LOTS of dividends from MORL BDCL & NEWT!) and it appears the 200-day moving average is the new line in the correction sand. (NEW updated buy under and portfolio I promise!)

But here’s the deal: In the first part of the April newsletter, I said “corrections on average last 6 months (bottom to previous high)” which means July. I said “we still need the scary gut-wrenching big volume capitulation of the LAST money into the market from the January melt-up and at least ONE 25+ VIX fear explosion.”

Key Point: YOU HAVE TO EXPECT more tests of the 200-day while this correction plays out. WE NEED to have a 25+ VIX to shack out the marginal buyers in Dec/Jan who are now the marginal sellers. We NEED the marginal buyers to step in a bargain hunt secular growth companies indiscriminately sold by S&P 500 index fund redemptions

Action to Take: We should expect some crazy trade war posturing and bluster. IF the craziness makes you crazy SELL SOME of your biggest winners and build more cash until your nerves are ok...OK? Note: IF you are a NEWT owner from 2015-2016--Don’t EVER sell those shares--with your stock dividends received you are getting at least a 30% cash-on-cash dividend from that investment!!! We ONLY shed shares when we are heading into the next recession.

The reality is EPS earnings will grow 20% this year and at least 15% next year PURELY on lower tax rates and $1+ trillion of massive stock buybacks and with 100% equipment expensing we will see 20%+ higher cash flows (with higher equipment expensing and less amortization).

I’ve made this point a LOT during our last 5 years together: the REASON we as equities and options investors GET TO double our portfolio’s on average every 2.56 years (and sometimes faster) in bull AND bear markets is:

1. We can take the brain damage of the normal volatility in a bull market cycle: higher highs and higher lows are how healthy bull market roll--there are NO higher highs without new higher lows! People who cannot take bull market volatility buy bonds--and they get the guaranteed minimum return without volatility. The brain damage comes in 1-3 month spurts like Feb-May 2018.

2. We are LONG the equities market as LONG as our TR MacroMarket index says “no risk of recession in next 4-6 months.” That has made us a BUYER of the scary fearful but regularly scheduled nervous breakdowns that wash out weak hands aka <30 relative strength corrections.

3. We HOLD our positions into corrections and hedge positions when >70 RSI aka over-bought IF the sector and leadership story is still intact. Our index is at 17.2 for May--2% chance of recession in next 4-6 months.

4. The GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2018 is 4.1 percent on May 1. NY Fed model is 2.97 so our blended GDP estimate is 3.5% for Q2018.

5. We do not panic or get emotional during normal health market corrections and sell into panic sell-offs when there are temporary or transitory exogenous fears in the macro-economy (with the exception of TRADE WARS--they are transformational but NOT in a good way--see my Final Word)

6. We continually identify/analyze and cherry-pick only the MOST transformational sector waves and stocks/ETFs in the market to “ride.”

7. We kick OFF those transformational waves when they run out of steam or get TOO far ahead of reality (like oil E&P and MLPs stocks in September 2014 when OPEC declared war on US oil share production or Impinj PI/Ambarella AMBA/Cavium/Mobileye when they rocketed too far too fast or OLED when iPhone X proved to be a dud for a new wave of OLED screens in

8. We go 150% defensive WHEN our Transformity MacroMarket Index tells us the odds of a recession in 4-6 months are 75%+

9. We re-enter early cycle sectors and the most blown-up top quality secular disruptors/high flyers when our MacroMarket Index flashes bottom in economic contraction.

10. We ride the fastest growing transformative sectors and their IP/Platform leaders HARD during expansions (and add to our gains “buying the dips” with long term options

11. We PROTECT/Hedge our bull market profits when one of our stocks gets ahead of itself >70 RSI or up 200%+ going into earnings (latest example our Micron Sell $162 Calls/Buy $158 Put Option Play).

12. We use HIGH-INCOME ETFs/BDCs/REITS to provide 20% annual returns and “ballast” to our aggressive growth plays & ADD High Income REITS/Leveraged Long Bond ETFs when business cycle starts to contract and interest rates contract/bond value expand.

THAT is the Transformity Investing formula: I suggest you print this out an put it close to whatever PC or laptop you use to execute your transactions!

The Semiconducter Space

I thought the good news from the memory chip giant Samsung (memory demand strong), AMD and Nvidia (GPU chips and Intel deals strong), Texas Instruments (Not iPhone impacted) and Intel (data center/data center/data center strong) got the semiconductor world off the snide from the Taiwan Semiconductor foundry slowdown for wireless chips. Then Facebook earnings blow-out and GOOD guidance (grrrrr) scared the shorts to death. PS: I talked with my option gurus CNBC’s Jon Najarian and others and we figured out how I should have hedged the FB rebound play...expensive lesson learned (should have hedged with WEEKLY put options and let the monthly May 4’s run--doh!)

BUT even with our long semiconductor positions UP over 15% in two days...this self-loathing market could not make its mind up. Right now we know the following:

1) We have re-tested the 200-day in almost ALL our 200-500% semiconductor winners from late 2015, 2016 and 2017

2) The Semiconductor Index looked like it is ready to roll-over any day but it held like a champ.

3) AVGO/Broadcom--a stock that we don’t own but is a bellweather for all kinds of chips has rolled over and has a set of lower highs since its December peak

Update 2018 Portfolio Strategy: The Known Knowns & Known Unknowns

Headwinds

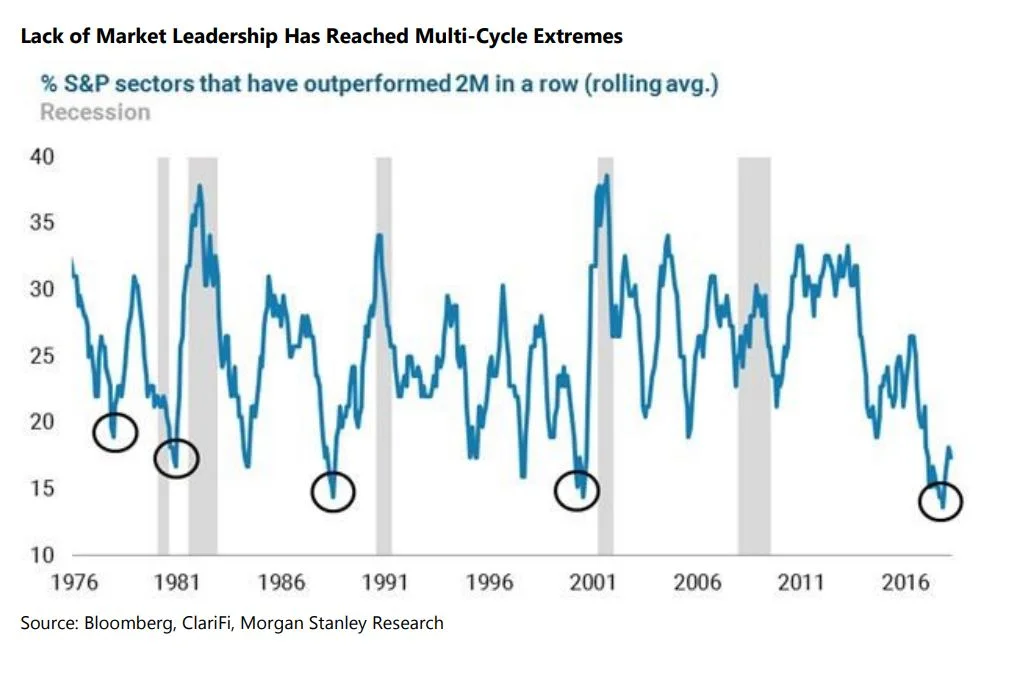

1. The U.S. stock market has obviously been stuck in a tight trading range for weeks, and a key reason for that may be simple: it has no leader to follow. Statement of the obvious: compared with 2017, when broad-market gains were particularly pronounced in technology stocks, there has been a pronounced breakdown in leadership thus far this year. “Rarely have we experienced such low leadership,” wrote Michael Wilson, chief U.S. equity strategist for Morgan Stanley, which estimated the percentage of S&P 500 sectors outperforming for two months in a row recently hit multiyear lows.

The top-performing sector is consumer-discretionary, up 5.5% in 2018. However, those gains are largely attributable to Amazon & Netflix. “Our experience tells us that these leaderless periods typically occur during important transitions in the market,” he wrote.

1. Investors are starting to fret about the strengthening dollar. The U.S. Dollar Index has risen 0.3% today, and is up 1.8% this month. The issue of course is a rising dollar makes U.S. exports less competitive and also it also hits commodity prices (that trade in dollars--which is EVERY commodity basically). Materials and industrials are two of the hard-hit sectors today.

2. The steel industry in Europe and a handful of other American allies could face new tariffs as of midnight, after an exemption period expires, The Wall Street Journal notes. Negotiations to avoid that scenario don’t appear to be making progress. “The EU has vowed to retaliate against American exports, including bourbon and blue jeans, though any action may not be immediate,” the Journal writes.

3. : That it slash $100 billion from the $375-billion annual trade deficit with the The New York Times writesMeanwhile, China is refusing to even discuss the Trump administration’s two boldest demands, U.S., and that the government limit its financial backing for industrial upgrades. “Beijing feels its economy has become big enough and resilient enough to stand up to the United States,” the Times writes. U.S. negotiators are to meet with their Chinese counterparts this week.

Key point: IF One wondered about the Trump administration about a well-thought-out plan in place for its trade battle, my friends at Axios recently reported that when the president called for $100 billion in new tariffs on China a few weeks back, he did so pretty much off the cuff. “There wasn’t one single deliberative meeting in which senior officials sat down to debate the pros and cons of this historic threat,” the publication writes. “Trump didn’t even ask for advice from his new top economic adviser, Larry Kudlow, instead presenting the tariffs as a fait accompli.”Shocking...just shocking the leader of the free world would freelance a trade war with China off his golden cuffs.

4. We have reached peak high end smartphones replacement cycle. The growth is in cheap smartphones for the masses in India and China. Shares of chip giant Broadcom (AVGO) are flat after the company this morning narrowed its forecast for revenue in the March quarter, saying sales into the data center were “robust,” but the market for wireless chips was “weak.”

5. Apple understands this reality and I forecast they KILL the X phone as a limited market phone

6. OLED and facial recognition technology are still too expensive for value priced phones (which is WHY we sold OLED but hold AMAT as the answer for high prices is MORE volume)

7. DRAM memory and SSD (solid state storage) are driven by ever larger data center storage growth (and quest for ever lower data center power bills)

8. Semiconductor manufacturing equipment is being bought for the transition to 10nm and 7nm semiconductor wafers plus the transition is unstoppable for 3D memory and other semiconductor chips. Especially strong are the two EUV makers: ASML is far and away leader and ACLS is still a buy under $24

Financials: FINU Buy Under $95

Earnings season has been unkind to bank stocks, but not their bonds. In the long-run, trust the bonds. Financial shares have trailed the S&P 500 Index in every session since JPMorgan reported results last Friday, with the industry falling to the lowest level relative to the market since November. In contrast, bond investors are taking the earnings in stride, with the extra yield demanded on investment-grade debt offered by financial firms over Treasuries hovering near a four-week low.

While concern over loan growth and trading revenue is lingering, analyst estimates for coming quarters show no signs of a slowdown. Profit growth will stay above 20 percent and accelerate to 28 percent in the final period of the year, data compiled by Bloomberg show.

Something’s not quite right with chip equipment stocks. ASML (ASML), makers of the cutting edge lithography equipment used to make the most advanced chips, is down $4.88, or 2.3%, at $207.82, despite an upbeat earnings report and outlook this morning, echoing the decline in shares of Lam Research (LRCX) last night, after that company also beat on both report and outlook.

In our view, this quarter shows that both cycle trend and EUV momentum are moving in the right direction. LAM and ASML are both positive on the 2018 cycle, driven by both DRAM and logic spending, which are both positive for ASML. Mehdi Hosseini with Susquehanna notes that the best part of ASML’s report was that its sales outlook for its tools "has remained unchanged at 20 (new) system shipments in 2018 and at least 30 (new) systems in 2019."

Intel Corp. reported a blowout March quarter led by strong growth in its data-centric businesses, but questions remain regarding the sustainability of the company’s results as well as issues with 10-nanometer chip production. “We think consensus was expecting strong results, but these were truly impressive,” wrote SunTrust Robinson Humphrey analyst William Stein. Intel beat earnings and revenue expectations by a wide margin on Thursday afternoon and reported 25% growth for its data-centric businesses, excluding McAfee. Data-related revenue accounted for nearly half of Intel’s INTC, -0.60% total sales for the quarter, a company record.

AMD is STILL A buy under $11

Advanced Micro Devices is on a roll with chip releases, the likes of which it hasn’t achieved in more than a decade. On the back of solid and consistent execution, the Ryzen 2000-series of PC processors launches this week and addresses several critical consumer markets. Previously called the Pinnacle Ridge platform, this new family of processors is aimed at the DIY (do-it-yourself) and personal computer (PC) gaming markets, in addition to computer manufacturers such as Dell and HP. The chips offer a better value and performance alternative to Intel Core-series, which has a dominant market share.

Rising market share

But the company is making strides. AMD claimed as much as a 50% share at component-specific retailers in 2017 and a resulting rise in market share to 12% in the fourth quarter from 9.9% a year earlier. Early reviews of the new chips indicate performance and feature improvements are solid over the previous generation and outperform the latest offerings from Intel in specific multi-tasking workloads. This is considered a “minor revision” of the previous chips, to tweak and perfect the current architecture rather than completely revising it. That is a task assigned to the “Zen 2” products coming in 2019.

Ryzen PRO family over the past year, AMD has launched dozens of new products in the processor and graphics chip markets. Those include the first-generation Ryzen processor, the business-targeted and the enthusiast-class Ryzen Threadripper,which pushed performance ahead of what Intel offered in the same category. In the server space, EPYC brought AMD back in the discussion for data center processor sales, an area it had dropped to nearly 0% share. HPE, Dell, Cray, Microsoft and others have announced EPYC-based deployments. Ryzen Mobile created a product for thin and light notebooks with several technology advantages that can challenge Intel’s dominance in that part of the market.

Competitive in graphics

In graphics, AMD launched several consumer and professional products based on its Vega architecture, bringing the company back into the competitive world of high-end gaming. Nvidia NVDA, -0.65% maintains market share leadership, but AMD is back in the game. Its Radeon brand gained more than 10% revenue share in discrete graphics chips last year, though how much of that is a result of cryptocurrency trading is up in the air.

Net-Net: Buy Under $11 with $16 Target

I'm going to let the new GDP and wage growth numbers come out tomorrow to update ALL the other positions with buy under.