AMD All the Way + Quick Update

Our 3X AMD Position up 92% in 2018--new target $23-$25

Dear Subscriber,

One of the key parts of our Transformity Alliance research process is working with analysts that I have found to REALLY understand our companies and the transformational products and services driving their value creation. Analyst Matthew Ramsay at boutique bank Cowen has been right on AMD since we first started looking at their pipeline cites the strong Q2 results, “de-risked” 2H18 outlook, and a meeting with CEO Lisa Su.

Says Ramsay on the conference call by CEO Dr. Su’s message was "AMD is just getting started; we agree.” Make that three. The pipeline is FINALLY hitting the street with Rysen server chips and new Epyc GPU that has closed much of the gap with Nvidia. AND let us not forget that AMD has beaten Intel giant at getting to lower energy consuming 10mm and now 7mm. AMD 7nm products launch later this year compared to Intel’s (NASDAQ:INTC) late 2019 release for its 10nm chips--as my old CEO used to say "stole a march."

Revenue breakdown: Computing and Graphics revenue was $1.09B (+64% Y/Y, -3% Q/Q); driven by strong Radeon sales and continued growth of Ryzen with the sequential drop coming from lower GPU revenue from blockchain. Enterprise, Embedded and Semi-Custom segment revenue was $670M (+37% Y/Y, +26% Q/Q) due to higher semi-custom and server revenue.

The new Epyc product sales are now rocketing higher against lower GPU sales in the blockchain market. Enterprise, Embedded and Semi-Custom segment revenue was $670M (+37% Y/Y, +26% Q/Q) due to higher semi-custom and server revenue.

Our biggest Transformity Sectors: HyperDatacenters? AMD is beating Intel in incremental sales. AI? AMD #2 to Nvidia. Gaming consoles? AMD now even with Nvidia. PCs and Laptop sales are up miraculously (corporate tax cuts helped here for sure) and this upgrade cycle has AMD CPUs and GPUs in alll the major PC makers all over the world.

Net/Net? Cowen expects AMD to generate EPS of $0.82 in 2019 (consensus: $0.62). We have AMD at .85 in 2019 and new price target $25.

Action to Take: BUY UNDER $18.50. IF you want to lower your cost again (and add some income) let's wait for other analyst upgrades Tuesday and Wednesday and THEN sell some pricey short-term call options. IF you are uncomfortable with our 3X weighting (i.e.,too much exposure) sell 10-20% of your position for building cash and "sleep at night". $17 is a VERY strong floor now...and as mentioned...guidance is higher for the next two-three quarters as AMD moves market share to high single digits.

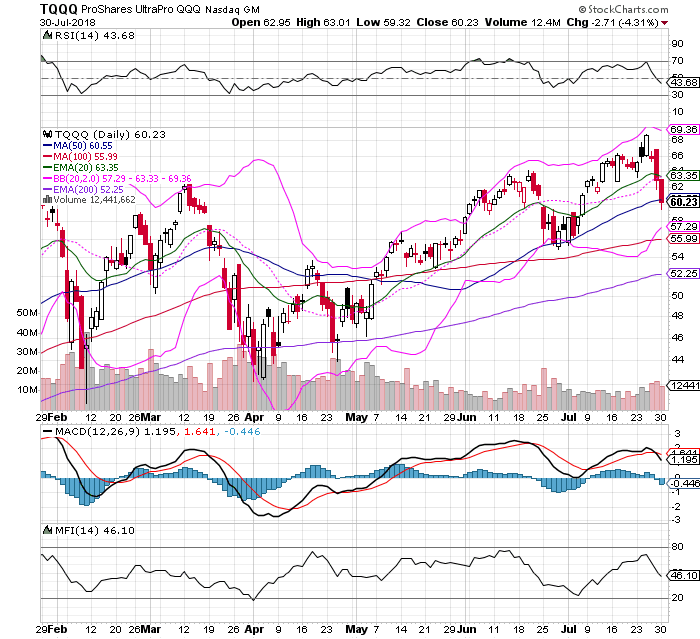

TQQQ

Our Buy Under $55 holds. We are back to support before Apple and other key components report. Facebook IS changing its business model to clean up its ad and content problems---that will mean some pain for a few weeks. But it is just starting to monetize its one billion users of Instagram and still have NO monetization on WhatsApp. There ability to target users by zip/politics and IF the user has purchased something on the FB or Instagram platforms. There is nowhere in digital advertising that an advertiser can pitch a user based on their buying behavior--that is still a big big advantage.

Newsletter out after Apple earnings. NEW 15%+ income plays to build our income-to-growth ration up to 40% high income (dividends which I STILL want you to reinvest if you have 5+ years till you need the income. NEWT is a great example of this--with dividends and $4.65 one time stock dividend us early investors have our share cost below $8. That is a 30% yield cash-on-cash AND we are sitting on a 105% capital gain on our shares. THAT is the advantage of dollar cost averaging your dividends into new shares.

Congrats to all the AMD owners!--more profits to come.