March Newsletter 2019 Part 1

Why Our Two Sectors--Bond/Utility Proxies & High Margin Secular Growth Tech are the #1 Performing Sectors in 2019

Dear Subscriber,

This is first of two newsletters for March. But first, if you have NOT printed out last month's February Newsletter--I strongly encourage you to print it out (it is now posted--our webmistress Stephanie is back and healthy--yea!). I stand by the forecasts and my comments on them for the rest of the foreseeable 2019--including the now penitent Fed and Fed Chairman that, just like in late 2015 and early 2016, acknowledge they jumped the gun on interest rate hikes because of their old "Fed Model" being "for shite" as my Northern Irish relatives would say.

Now this is not to say that we do not monitor the slowing Europe expansion (or contraction in Germany) and the bizarre real estate credit bubble in China were 80 percent of Chinese wealth is in residential real estate and yet 65 MILLION apartments stand empty and most will never be occupied. Or that real Chinese levels vs. GDP stand now at an astonishing 244% of GDP. I will never forget visiting a vacant city with 50,000 empty apartments in China--it looked like a bad digital CGI vision from a zombie movie. Debt is crack cocaine in China--they are addicted to it. BUT--what most Americans (other than you) don't understand is that Chinese households SAVE 40% of their take-home pay--so they own almost all that debt. You can't foreclose on yourself--you can lose all your equity in one of those 65 million apartments--but yet in the big four cities of China--Shanghai, Beijing, Tianjin, and Shindou (with an average of 15 million citizens a piece --oh man!) apartment values continue to expand. The PRC just creates more money for the "Grey Rhinos" aka the private non-bank lenders that pay high yields relative to PRC bank deposits. One day there will be a real financial asset reckoning --bu as long as the PRC Central Bank has a button to push that creates electronic cash, that day ain't today.

We follow China closely--again both they and Mr. Trump must settle the trade war quickly to keep both countries from a recession. in 2019.

Note to Chairman Powell: if you want to make an accurate real-time forecast where the economy will be and not where it has already been, you can strongly supplement your random guess track record inaccuracy by listening to the most sophisticated real-time survey in history on the direction of growth, inflation and monetary policy-- try looking at the real-time prices of 24/7 traded financial assets!! They are shockingly highly sensitive to changing expectations of the current and future trajectory of --wait for it--GDP growth, inflation and yes monetary policy you knuckleheads! What do those hundreds of Ph.D. economists do there all day--play Fortnite on huge TV screens?

Moreover, the Fed has been overoptimistic about quarter-to-quarter future GDP growth for every quarter since I started following the Fed forecasts--in 1982! The Fed's October 3 missive that "We are not close to neutral rates" and then December's "the $50 billion a month unwinding of QE (read runoff of debt securities) is on auto-pilot" ) went over like a $9 trillion lead balloon ( and to his credit, they did finally move quickly to fix their #^$#6 up. But credit spreads over Treasuries for low rated debt and commodity prices have still not recovered BTW--so the credit and commodity markets are not believers in no 2019 recession yet).

Mr. Powell finally acknowledged in the March meeting last week what myself and other macroeconomic model makers have acknowledged for the years after the Fed embarked on "Quantitive Easing" aka injecting $3 trillion of electronic cash into their major members banks to make real US bond yields negative (after inflation) meaning you paid the Fed to lose money.

What they created was a self-reinforcing positive economic feedback loop for secular fast growth risk assets (which we have owned since 2013 and its how we have earned over 53% a year since 2013) and now, with global growth slowing significantly, makes "bond/utility proxy" assets with 10%+ yields attractive to in essence hedge the extra volatility of risk assets in a low liquidity world (low liquidity relative to past decades because the biggest marginal financial asset buyers aka top 10 banks have much stricter house-trading accounts and liquidity regulations). Conversely, when the Fed tightened short term rates above the long term rates of every other major economy, a positive feedback loop was created for longer term 5-10-20-year US Treasuries that kept those yield rates artificially low/prices high.

This is how we now find ourselves in the infamous "inverted yield curve" where short term 3-month yields exceed 10-year yields--and why we have 12-16 months of more stock market gains before we pull back and protect our 7 years of 50%+ annual profits and dividends.

BTW--we use the weekly and monthly yields of three month and one-year treasuries in our MacroMarket model to smooth out the daily yield curve for forecasting reasons.

Action to Take: We will need to use the 2019 recession fear market pullbacks to add to some positions and diversity into more subscription based software-as-a-service leaders to own the 'growth bond proxies" of world largest secular technology shifts--to 5G mobility, Autonomous vehicles, Datacenter cloud-native computing, gene-based biotech medicines, and AI/Machine Learning/Big Data based commerce and robotics. Plus some corporate transformations and special situations.

Look folks--the "yield curve" is not mysterious. It is simply two lines line plotting out yields across Treasury debt maturities. Typically, it slopes upward, with investors demanding more compensation to hold a note or bond for a longer period given the risk of inflation and other uncertainties. An inverted curve could mean short-term rates could be running high because overly tight monetary policy is slowing the economy (bingo!) or it could be that investor worries about future economic growth are stoking demand for safe, long-term Treasurys, pushing down long-term rates, note economists at the San Francisco Fed, who have led research into the relationship between the curve and the economy.

They noted in an August research paper that, historically, the causation “may have well gone both ways” and that “great caution is therefore warranted in interpreting the predictive evidence.”

The 3-month/10-year version that is the most reliable signal of a future recession, according to researchers at the San Francisco Fed. Inversions of that spread have preceded each of the past seven recessions, including the 2007-2009 contraction, according to the Cleveland Fed. They say it’s offered only two false positives — an inversion in late 1966 and a “very flat” curve in late 1998.

#1 Our fearless and deadly accurate Transformity Research MacroMarket Index stands at 15.5--14% AWAY from a 4-6 month recession is coming warning. The blend of the Atlanta and NYC "Nowcasting" GDP forecasts (we have modeled both--and just by blending their separate models it has been very accurate GDP forecasts).

#2 The Latest Q1 2019 GDP Forecast: 1.25 percent — March 22, 2019

The Atlanta Fed GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2019 is 1.2 percent on March 22, up from 0.4 percent on March 13. The New York Fed Staff Nowcast stands at 1.3% for 2019: Q1 and 1.7% for 2019: Q2. First quarters have been squirrely since the advent of e-commerce and climate change which has thrown post-holiday shopping, construction days and crappy weather into Q1 GDP forecasts (and makes them subject to big revisions later in the year).

Key point: An economic recession is not on the immediate or longer-term horizon in the United States. Nor is a bear market. The reason is simple--yield curve is a FORWARD indicator with a 10-14 month lag time. Think about it--did you suddenly sell all your stocks and start buying dried food on Friday? I certainly hope not. You have to look at the mitigating issues first. First--in the aftermath of quantitative easing all the major global central banks own a majority of US government bonds. Since so many Treasurys are held by central banks, the yield can no longer be really seen as market-driven--there are too many idiosyncratic reasons not related to the actual real market demand for bonds to freak out about a two-day yield inversion.

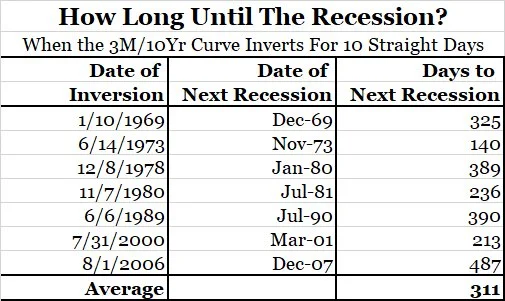

Meanwhile, recessions in the past have typically come around in about 300 days after 10-days or more of inversion occurrence. Data from Bianco Research shows that the 3-month/10-year curve has inverted for 10 straight days six or more times in the last 50 years, with a recession following, on average, 311 days later.

Per @biancoresearch the 10-year/3-month curve has inverted for 10 consecutive days or more 6 times in the last 50 years. On each of those occasions, a recession has followed (on average 311 days later).

Until we see our key recession indicators aka the unemployment rate, and jobs growth starts blinking red, it’s simply premature to press the panic button. Lets also not forget with all its data on the recessions that follow inverts, the Fed is eager to avoid inversion of the yield curve that is longer than a quarter. The Fed rate futures already point to LOWER Fed Funds rates by November--that is one way to end the inversion--albeit with a hammer. And let's use HYG High Yield Bond market as our "recession fear proxy" vs. the Fed Funds rate--if the high yield bond guys see real evidence of an oncoming recession in the US--the high yield market will tell us first.

So that was a lot of words to say "We are in the last 12-15 months of this expansion" in a world that is slowing in growth rates which should continue the Fed's desire to never have a recession again in the United States."

Our strategy--a balanced "barbell" of secular growth stocks that have subscription-based business models or large advanced standing order books on very high margin semiconductors or other 21st-century enabling technology. Software-as-a-subscription has become technologies port in the storm. With the transformation of legacy enterprise software applications to cloud-native applications is only 25-30% complete. With the inherent risks and additional fixed costs of corporate data centers, only a handful of large companies (defense and military industries) will keep their own data centers. Marc Andresson's proclamation that "Software is Eating the World" in 2011 has been dead right and the costs of not converting to cloud-native applications become higher every year.

On the "marketing tech" or Martech side is Salesforce.com (CRM) at the top. On the productivity subscription and cloud computing and business analytics side is Microsoft.

I have been patiently waiting for another pullback to build a mini-portfolio of four more to add to our big SaaS winner Chegg (who is not in the enterprise space as you know). We are working on a new valuation for CHGG--these SaaS stocks that deliver quarter after quarter of "Beats and Raises Guidance" are NEVER EVER cheap. But we did get a nice pullback to the $37 50-day on profit-taking. I'll increase CHGG buy under to $37.50 with a $46 target.

All position updates and new SaaS and High Income Play this week.

Stay positive--we still have a fair amount of cash that we can deploy.

Don't fall for the "4 Horsemen of the Apocolypse" newsletter ads you will start seeing now with the inversion--especially the Harry Dents and John Hussman's of the world screaming a "75% correction coming in 3 weeks" BS.