April 2017 Newsletter

I’m going to talk economic and political realities this month and come back next week with some new secular growth sectors for us to get into.week with some new secular growth sectors for us to get into.

I’ve upped the buy under prices on most positions and I HOPE from the last time upped Buy Under’s you got some/added to Imping (PI), OLED, AMBA, AMD and NRZ since they are all up VERY nicely.

Action to Take: Our positions are a HOLD here until we get a majority of our earnings reports in. So far out positions are killing it with LRCX and others beating and raising guidance (this is the whole point of investing in secular growth sectors and leaders…the beat conservative guidance again and again.)

The Reality of Trumponomics

I’ve been advising you since January that the irrational exuberance behind the delusionary Trump Bump was a game of chicken: I asked “who would blink first?”…the Trump believers looking for massive fiscal stimulus from tax cuts, deregulation and $2 trillion in cash repatriation from the gang that can’t legislatively shoot straight OR realistic equity portfolio managers with equities bid to valuations that had priced in an extremely difficult political transformation in a system designed on purpose by our founding fathers for incremental changes at best.

Well the rational adults did not blink. The stock and bond markets were well into pricing OUT TrumpCare, major Trump/Ryan Tax Reform + $2 trillion in cash repatriation + 20% Corporate tax rates since mid-February.

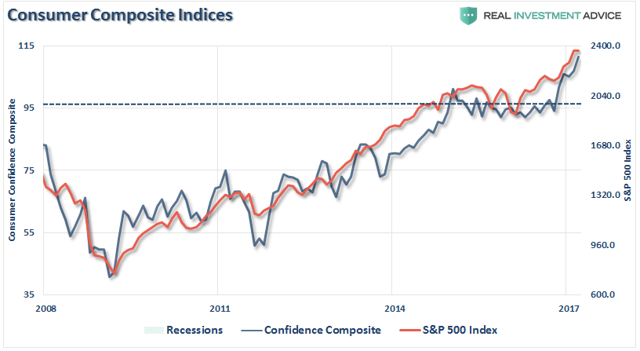

BUT—as I learned in my first year on Wall Street—“The Market sees and hears what the Market sees and hears.” In short, if the market (as measured by S&P 500 index cash inflows) sees blue skies and cupcakes (as measured by economic sentiment data and cash inflows into long positions) the market is going to go up.

Thus with the end of the French populist candidate in its election run-off and relief rally…and Trump’s 15% corporate tax riff including ALL business “pass-through” entities like LLCs, MLPs, Sub-S corps etc. PLUS a strong beginning to earnings season, the equity market still LIKES what it is seeing and hearing WHILE the bond market does not buy Trumponomics one bit.

The market is clearly overpricing the Trump agenda as if it will ALL be enacted…and that makes our job to RIDE THIS WAVE of misplaced optimism for as LONG as it lasts.

Sentiment still is driving stocks…for now.

Look at how much $$$$ riding this sentiment wave has made us in the first 4 months of 2017:

Key Point: As I have shared since January, the US stock market has become a “Trump On, Trump Off binary trade. I am not alone in this simple analysis: Boris Schlossberg, managing director of foreign exchange strategy at BK Asset Management, is one of those strategists who has in recent weeks noted that all trades have become political, for precisely these reasons. In a new interview, he said market bulls are now essentially making a "binary bet on Trump and nothing else."

I agree. .02% GDP in Q1 and 2% or less Q2 GDP growth do not reflect the continually weak real economy in general stock prices (except for OUR secular not cyclical growth stocks that are NOT dependent of the fantasy of 3-4% GDP expansion). 50% of EPS gains for SP 500 index for Q1 are coming from energy companies and financials coming off horrible Q1 2016 comps and now deteriorating fundamentals (oil prices and 10-year/2-year bond yields).

Our Latest US Q! GDP forecast: 0.2 percent — April 27, 2017

The final GDPNow model forecast for real GDP growth (seasonally adjusted annual rate) in the first quarter of 2017 is 0.2 percent on April 27, down from 0.5 percent on April 18. The forecast of first-quarter real consumer spending growth fell from 0.3 percent to 0.1 percent after yesterday's annual retail trade revision by the U.S. Census Bureau. The forecast of the contribution of inventory investment to first-quarter growth declined from -0.76 percentage points to -1.11 percentage points after this morning's advance reports on durable manufacturing and wholesale and retail inventories from the Census Bureau. The forecast of real equipment investment growth increased from 5.5 percent to 6.6 percent after the durable manufacturing report and the incorporation of previously published data on light truck sales to businesses from the U.S. Bureau of Economic Analysis.

Reality is we will not know ANYTHING about the final form the Trump Tax Reform plan until August at earliest. ONE thing ALL sides do agree on is cash repatriation…who could be against that?

Key Point: My best guess right now is the lion of “Trump Tax Reform” ends up a much less aggressive mouse: It keeps 10% cash repatriation holiday, gets rid of the 15% rate for pass-through vehicles (or severely restricts its use to dodge income and self-employment taxes) and we get three brackets and call it a day.

NOTE: As an owner of many LLC entities, IF I could have my earnings taxed once at 15%...OMG…and write off LLC entities with tax losses against LLC income and pay just 15% of the remainder I take back every nasty thing I ever said about El Trumpedo.

Here our quick and dirty analysis of Trump Tax Reform sans the dirty details: Virtually ALL the one page “wish list” presented last week by the Trump White House is DOA in the Senate with OMB scoring of $5-8 trillion in additional deficit spending.

The White House says “increase GDP with pay for the tax cuts: We call Bullshit.

he wishful economic thinking at the White House comes from "Dynamic Scoring” . . . the method of economic forecasting that predicts the impact of fiscal/tax policy changes by forecasting the spending/investing effects of consumers and business reactions to economic incentives created by policy.

The OMB method is "static scoring" that does not add assumptions for GDP growth from incentives or "multiplier effect" assumptions other than simple addition and subtraction of cash flows.

The Alternative Definition of Dynamic Scoring in 2017 : "Spreadsheet Masturbation"

Key Point: ALL you are going to hear and read about regarding Trump Tax Reform in the next months will be based on White House quants using" dynamic economic incentive scoring" and “supply side economics” to essentially say "Our tax cuts will pay for themselves with higher GDP growth that we assume happens when consumers & companies have more after tax income to spend/invest."

In the 80's this concept was called "trickle down economics" aka the Laffer Curve (thesis that lower marginal tax rate is highly correlated to higher GDP) aka “supply-side economics.” Well I won’t go into ALL the reason how the actual empirical reality has categorically disproved “supply side economics” but here is the bigger problem: after two stock market meltdowns and one Great Recession, Americans for the last 9 years have used tax refunds/tax savings to mostly pay down DEBT and build savings and not go on a spending spree. Supply side is based on the assumption that if you put an extra $dollar in a person’s pocket they will spend it.

The other problem/efficacy issue of course with trickle down economics is where you start to trickle down from. JFK had 90% top marginal tax rates…his marginal tax cut to 70% was huge. Reagan took 70% highest marginal rate and took down to 36%...huge...and got rid of non-economic tax shelters...huge.

Taking highest marginal rate in 2017 from 39.6 Federal to 33%...NOT HUGE. Incremental or marginal at best. NO "trickle down' effect.

#3 Problem: In JFK and Reagan era workforce was GROWING and for Reagan Baby Boomers were just starting to move to peak earnings cycle i.e., the GDP tide was moving IN.

#4 YOOOGE problem: the US demographic tide is moving OUT not in. TODAY macroeconomic reality is that ANY positive GDP effect from lowering marginal rates to corporations (who used to pay 30% of US tax revenues but only pay @10% of Federal taxes collected now) and adding deductions so that 60% of US taxpayers pay ZERO income tax (20% highest income households pay 92% of income taxes already) cannot POSSIBLY mathematically offset the GDP reducing drag of what I call

The 12 Pillars of Secular Lower Rates of US GDP aka the GPD tide permanently going OUT circa 2017-2027:

- 16,000 Baby Boomers are turning 65 or 70 EVERY DAY (6 million a year!) with much lower household income and MUCH less consumption ex-travel and healthcare. They are being replaced by 82 million Millennials/GenXer’s who are marrying 6-8 years later and having kids 8-10 years later than Boomers. In short, they are not replacing lost Boomers spending and household formation NEARLY enough to overcome the 16,000 Boomers turning 65 or 70 every day.

- 15% of adult population is >65 vs. 8% in Reagan era and rising to 20% by 2027

- 92 million Americans (out of 334 million) are NOT in workforce at ALL via a)retirement, b) students in college, c) stay at home parents d) stay at home caregivers e) incarcerated f) on SSI disability g) drug addicts or not able to pass a drug test. In 1986 72% of population was in work force...today 63% of 16-65 year olds are in the labor force and trending lower.

- 18-22% of men aged 25-54 in U.S. are out of the workforce permanently (disability, incarceration, opioid addiction etc)

- The biggest job creators in US last 5 years were energy & healthcare...BOTH of which have slowed significantly. Today off-site drilling technology requires 40-70% LESS roughnecks on a drill/frack site. And the biggest growth sector in 2017 is technology, which creates 50-80% LESS jobs per $million of output vs. energy and healthcare.

- Retail Armageddon: With 16 million retail jobs going to 10-12 million over the next 8-10 years as 25% of America's retail stores go out-of-business and 40% of malls closed/converted.

- With immediate expensing of the cost of Robotic Automation in manufacturing and AI/Machine learning technology the permanent destruction of unskilled manufacturing and transportation jobs would ACCELERATE. In 1980 it took 25 employees to generate $1 million in manufacturing output. Today it takes 5-8 depending on the product.

- IF Pass-Through Entities (Sub-S, MLPs, LLC, LLPs) were taxed at only 15% rate and LLC owners were able to consolidate LLC taxable income against LLC losses PLUS take distributions at 15% rate rather than at personal 35% marginal rate, this move ALONE would cost US federal and state tax collections over $1.5 TRILLION a year in lost personal income taxes...and cut SS and FICA contributions by 200-$400 BILLION a year.

- 1986 Tax Reform moved pass-through tax LOWER than C Corp tax rate…and created a BOOM in Sub-S/LLC business entities. THE tax arbitrage of C Corp to S-Corp in this plan is TWICE as big as 1986--so an avalanche of private C-Corp's will convert to S-Corps lowering paid taxes by highly paid business owners ever MORE than 1986-1996

- Eliminating AMT tax, Estate Tax, and Obamacare 3.9% tax on high income households (in addition to 15% pass through tax) puts about @90% of ALL Trump Tax Reform tax benefits (total $$$) to the top 5% of American households ranked by income --ZERO Democrats in Senate would pass this. The same plan adds $5-$7 trillion to the US deficit in 10 years…FEW if any House Freedom Caucus members would vote yes.

- Past history of corporate overseas cash repatriation at 10% tax cut shows public companies (who hold 85% of all offshore non-repatriated cash) use on average 80%+ of that cash to BUY BACK their stock and pay dividends and not invest in new equipment or people.

- Unless there are HUGE restrictions on C-Corp to S-Corp/LLC conversions, they will become the biggest legal tax shelters in history. Owners are massively incented to take a nominal salary of $50k, shelter up to $225k of taxable earnings into a Defined Benefit pension plan, BUY LLC member interests in highly leveraged Private Equity LLCs with 2x-10X operating loss pass through and THEN take whatever cash is left as a 15% tax distribution. OH to be a CPA and Tax Attorney in Trump Tax Reform!

KEY POINT: The Trump Tax Reform plan is BASED on the economically IMPOSSIBLE assumption that it will raise US GDP 50% to 3% (from 2% in 2016) with fiscal stimulus of tax reform and THAT reduced regulatory burdens and corporate tax rate incentive would increase U.S. GDP 50% for the 10-year duration of the new tax bill.

To raise the U.S. economy to 3% GDP means adding @$570 BILLION in new GDP every year…$5.7 trillion over ten. Giving the economic realities listed above, the odds are ZERO as the math does not come close to adding up.

Our basic US macro-economic model at Transformity Research calls BULLSHIT on that assumption...literally impossible given the most SIMPLE math calculations.

Really Key Point: When the OMB scores this plan with STATIC vs. Dynamic macro-economic models or at best dynamic scoring models with non-fantasy economic multiplier assumptions, the magical thinking of Trump Tax Reform is DOA. The Bond market has made it clear they don't buy this magical unicorn. The devil is in the details of course. At the end of the day Trump Tax Reform looks like 1) Corporate Cash repatriation 2) same tax rate for C vs. Pass-through entities passes at 25% vs. 15% 3) Three simplified personal tax rates and higher simple basic deductions for all taxpayers.

IN addition, Trump has not only failed to understand the political dynamics within his own party – on both politics and policy, as Steven Nadler of the University of Wisconsin-Madison puts it, he is “ignorant of his own ignorance.”

My long time economist pal Nouriel Roubini makes the same call: Nouriel Roubini expects that efforts by Trump and congressional Republicans to reform the US tax code will share the same fate as the stillborn “American Health Care Act.” Roubini describes most of the reform ideas that were originally floated by Trump as “dead on arrival” even in a Republican-controlled congress. Neither a proposed border adjustment tax nor an alternative value-added tax has “enough support even among Republicans.”

“Even cutting the corporate tax rate from 35% to 30% would be difficult,” says Roubini, because it would require a broader tax base, “forcing entire sectors – such as pharmaceuticals and technology – that currently pay little in taxes to start paying more.”

On the other hand, if Trump and congressional Republicans “blow up the debt,” by cutting taxes across the board without making up for lost revenues, the “markets’ response could crash the US economy.” Ultimately, Roubini expects that the Republicans’ “roaring tax-reform lion will most likely be reduced to a squeaking mouse.”

But We Know This: The Bond Market and Oil Market Have Already Priced OUT Trumpflation—For Now.

The equity and bond market are in opposite corners of belief in Trumponomics. In the green corner are stocks. The Standard & Poor’s 500 index is just 0.2 percent away from a record high reached in March and Nasdaq Composite is >6000 on bets that Trump’s administration will push through tax-code changes to spark growth.

In the red corner sit U.S. government bonds, where benchmark 10-year Treasury yields have unwound almost half of their post-election increase, suggesting a far more pessimistic view the economy.

Who is right? Interest-rate markets are flashing warning signals. Money markets such as the London interbank offered rate and interest rate swaps, for instance, show some alarm over growth prospects next year.

“The rates market is pricing in the death of tax reform and dimming 2018 economic prospects,” strategists at Merrill Lynch led by Shyam Rajan wrote in a note to clients.

Yes the outcome of the first round of voting in the French presidential elections obviously brought a widespread relief rally (Viva Le France!) on the view that geopolitical risk is diminishing.

My best guess today: IN the short term bond markets were more worried about Le Pen, and the Treasury rally reflected flight to quality out of Italian & French bonds. What’s more, the outperformance of small capitalization stocks -- which tend to be more domestically focused than their large-cap peers -- has eased since late February, highlighting that equities, to some extent, are pricing in less enthusiasm over U.S. growth.

One big clue we both see: look at the chart of the London Interbank Offered Rate (Libor), a global benchmark for short-term loans, which shows market participants are projecting a steady decline in rates.

Put another way, the market is betting that the Federal Reserve’s rate-hike cycle is likely to come to an end in 2018 after just two more increases this year. That effectively prices OUT a fiscal spending avalanche from Trumponomics and prices in a mid-term election disaster for Trump and Trumpism.

Don’t forget the yield on the 10-year U.S. Treasury spiked (prices sharply fell) in the aftermath of Trump’s election on a belief that his pro-growth policies will lead to a rise in debt. It again surged in March when he released his budget proposal that notably boosted defense spending. Since then, however, the yield has corrected lower rather than pushing higher in line with the Fed’s tighter policy stance.

Tax cuts are dead? Well look at how the companies most likely to benefit from Trump’s tax cuts have surrendered their recent gains in the last month.

Key Point: The engine of the U.S. earnings recovery that’s underpinned stock gains this year is starting to sputter. “The rolling over of inflation expectations and commodity prices presents unique risks for sectors that were large contributors to better earnings expectations,” said Alex Bellefleur, head of global macro research and strategy at Pavilion Global Markets Ltd. in Montreal. “The risk is that markets begin to reassess the forward earnings picture and turn a little less optimistic.”

Key Point: This is AGAIN the reason we are invested in SECULAR transformational technology sectors and stocks that are NOT dependent on the success of Trumponomics. Oil prices are key for energy downward earnings revisions

Action to Take: The REAL transformational technology economy and real earnings are driving our stocks and investments higher…that is GOOD!

What About Infrastructure?

Optimism over an infrastructure boom is already fading. After surging 18 percent over the first four days after Trump’s win, the S&P Supercomposite Construction and Engineering Index has made little headway and is down about 6.6 percent from its December peak. There is ZERO chance of ANY meaningful infrastructure legislation in 2017....ZERO.

Action to Take: Stay with REAL transformative technology and the Apple 10 Year upgrade cycle. WE have also maintained that the $trillion of simultaneous technology transformations are “Trump Proof”…that whatever the Trump Administration doesn’t do will not affect the upward trajectory of the value of our leading enabling technology leaders.

5G is Coming!

WE are getting ready to invest in the 4G-to-5G transformation! On Monday, wireless telecom name AT&T (NYSE:T) gave us a not-so-gentle reminder that, ready or not, 5G connectivity is coming. The country's second-biggest wireless name announced it was acquiring Straight Path for a cool $1.25 billion, garnering a nice-sized sliver of spectrum in the process.

Straight Path owns 735 so-called millimeter wave licenses in the 39 gigahertz band of FCC-regulated airwaves and another 133 licenses in the 28 gigahertz band. That's a pretty wide swath of radio frequencies, but more important, Straight Path's licenses are in frequency bands needed by 5G networks, and geographically cover the bulk of the United States.

The announced acquisition comes just two months after AT&T said it was buying FiberTower, largely for the same reason... spectrum. That deal surfaced shortly after rival Verizon (NYSE:VZ) bought XO Communications late last year, mostly to garner its spectrum.

With several 5G network trials slated for this year and commercial rollouts expected next year, it's time to take the conversation to the next level. That includes some deeper critical thinking on the matter, and one of those "aha" evolutions of the conversation of the matter is an acknowledgment that Verizon and AT&T, as involved as they are, aren't the ideal ways to play the rollout of 5G. The telecom players are only investing in the technology because they know other names in the business are going to offer it to their customers. It's just another battlefront in what will be a price war.

Instead, it's time we shift focus to the companies that have largely been obscured by the noise, and will quietly be the key beneficiaries of the demand for the technology needed to make 5G a commercial success. That's Red Hat (NYSE:RHT) and Cavium (NASDAQ:CAVM) and Corning (GLW) each for their unique reasons.

Red Hat

Red Hat is known as a cloud-computing name - its OpenStack product is an industry favorite. It's also becoming a big name in server virtualization though, which is a key component of the 5G evolution, clearly the hyper-speed connections 5G speeds compared to 4G will make it easier and more feasible to use more cloud-based apps and tools.

Whereas the Internet of Things (iOT) has been fun to think about but of little consequence so far, when that data can be transmitted at 10 times the speed it's currently being transmitted, the world can feasibly start to gather the mountain of data that will make good use of the IoT premise.

This is why we like Imping (PI)…they enable the iOT)

Last quarter's impressive numbers were just the beginning. Red Hat CEO Jim Whitehurst flat-out said to Motley Fool contributor Anders Bylund in a phone interview following that report:

"A particular area of strength is telco network functions virtualization, or NFV. We did a couple of very large OpenStack deals. As telcos move toward 5G, they have to build up a whole new infrastructure to handle that kind of volume. I think that the general consensus is that this is going to be commodity hardware running OpenStack. Frankly, we've been saying all along that we're working to ensure that Red Hat is the, you know, Red Hat of OpenStack. I think we have made a lot of progress this year with large telco wins and telcos recognizing the value of having a standard OpenStack offering that all of their NFV providers and all their hardware providers have been certified to. So we're feeling really, really good about the traction we're getting with OpenStack."

Cavium

Of the two stealth names that could become big winners as 5G becomes reality, Cavium is the lesser known and arguably the bigger risk. But, with the bigger risk, you get greater reward.

Cavium makes and market processors specialized for networking and digital communications. The company's ThunderX server CPU, for instance, is a top-notch cloud and data center processor that's scalable and can be fully virtualized. Bank of America analyst Vivek Arya specifically noted the ThunderX when he pegged Cavium as one of the underappreciated ways to sneak into the looming explosion of 5G, reiterating a buy rating on CAVM earlier this month in saying:

"Specifically, we believe CAVM benefits as in 5G more baseband processing moves to the base station from traditional radios, given the high latency and limited bandwidth available in traditional (CPRI) standards that connect the radio to the base station."

Cavium has a whole suite of products and technology that will become the physical platform necessary to fully commercialize 5G. At stake is a piece of the $700 billion the likes of AT&T, Verizon, Ericsson and others will need to spend in the foreseeable future to upgrade their entire networks to 5G technology.

Final Word

I learned a long time ago in my Wall Street career "Dont let your politics interfere with investment judgement." I am sure out of a few thousand subscribers to NBTI Pro there are many Trump fans/voters.

MY JOB is to analyze and separate economic and political fact from fiction.

So DONT take our negative analysis on Trumponomics and Trump Tax Reform as a shot at your guy.. Like Michael Corleone said "Its just business."

Back in 7-10 days with our next stock investments for the second half of 2017.

- Toby

Copyright © 2017 Transformity Media, Inc., All rights reserved.