January 2017 Newsletter, Part II

The Stock Investor’s Analysis of Trumpism and Trumponomics on US and Foreign Stock Markets

Well…now let’s look at the biggest risks for 2017—they are key to our 2017 portfolio strategy. In general we will stick with our NBTI core strategy: stocks and ETFs with 28-30% upside potential derived from secular (not cyclical) transformations.

We know what the stock market wants most:

- Strong earnings reports from the 4th quarter that validate an economic rising tide

- Corporate income tax reduction by June-July (which boosts EPS and offsets strong dollar)

- $2 trillion in potential corporate cash repatriation (which means HUGE stock buybacks, higher dividends and incremental increase in capital investment)

- Daily destruction of anti-growth regulations and growth regulations adopted

- Major overhaul of banking and EPA regulations

- A replacement for ACA/Obamacare that does NOT leave 22 million newly insured without insurance coverage

- A new conservative business friendly SCOTUS Justice

- Possibly 2 new DOVISH Fed members to push out the rate hike hawks

- More favorable trade agreements to U.S. companies

- Hardline trade agreement re-negotiations

The biggest risk I see is IF Trump Team can be successful in the first 100 days at LEGISLATING (i.e, passing actual legislation not executive orders) we have a ball game. Obviously the Trump Rally rationale has been mostly binary to this point: Trumponomics is assumed to be very positive for U.S. GDP growth (fiscal stimulus for infrastructure and $trillions in offshore capital repatriation), higher after-tax profit margins (corporate income tax to 15%) and less capital investment constricting Federal regulation compliance burdens.

Starting last week the euphoria the early onset of executive orders met with the reality of the negative aspects of Trumpism . . . starting with the reality that the Trump administration is not really a “Republican” administration at all . . . its’ more like an ethnic nationalist administration combined with a cold hearted corporate mentality.

Key Point: We are stock market investors not politicians. Money has no morals or political beliefs. But to wit, picking a fight/threatening a trade war with our 3 largest trading partner Mexico, banning free travel from 7 Muslim majority countries (all of which we don’t buy any crude oil from btw) and adding my old friend Steve Bannon (who leads to the “America First, always America First” philosophical battle) to a permanent position on the life-and-death National Defense Counsel are all antithetical to traditional Republican free trade, open borders and non-politicized national defense policy.

This set of events has NOT gone unnoticed by the traditional GOP brethren. In fact, I am told by many friends on the Hill that the worst kept secret in DC is just how much Speaker Paul Ryan and Majority Leader Mitch McConnell outright HATE POTUS Trump. They are keeping a face for the cameras, but Trump’s promise to have a replacement for ObamaCare “very soon” that is “lower cost and covers everybody” was the last straw. THEY realize the GOP only gets ONE chance on this issue that now 65-70% of Americans don’t want to see (only those in the States like Arizona who lost all but one Obamacare plan “hate Obamacare”).

Ryan and McConnell live in the real world (not Trump’s imaginary bubble/alternate universe where whatever he “feels” is fact is his reality) and THEY know the words “lower cost” and “cover’s everybody” are a diametrically oxymoron (or I guess what we now call “alternative facts”).

As such, the “TrumpTrade” rally stocks we have avoided as “too far too fast” are beating a fast retreat back to pre-election values. Clearly some sober reality started to seep into the “growth and nothing but growth” post-election cyclical stock euphoria of a House/Senate/POTUS legislative and SCOTUS judicial majority.

Key Point: The market take away this week is that Trump is also capable of turning ethno-populist Trumpism into harmful-to-growth BAD policy, too. We are quickly entering “Stage 3” of market reaction to Trumpism with the following questions:

- Is the Trump administration going to create permanent chaos in the White House/GOP (it should be noted that Mr. Trump loves chaos…his business management style has always to been create organization chaos and see who rises to the occasion) and

- How effective will the Trump Team be in getting Democratic Senators on board with Corporate and Personal Tax reform? Issuing executive orders is easy and is not legislating—without 8 Democratic Senators to vote with the 52 GOP Senators on Trumponomics promises (tax reform, capital repatriation, 15% corporate income tax rate) Trumponomics promised legislation will NOT pass the Senate (i.e., won’t get a vote in the Senate).

However, IF Majority Leader McConnell successfully removes the 60 vote filibuster block back for Supreme Court nominee to simple 51 vote majority(the so-called “nuclear option”)THEN all hell break lose and Dems could easily go a filibuster warpath (there is no nuclear option for legislation…for very good reasons).

The risk in the capital markets is U.S. tax reform gets hung up by Republicans who are from States/districts that did not vote Trump or are traditional GOP fiscal conservatives…i.e., they want spending cuts to roughly equal tax revenue cuts.

Trump continues to play to his ethnic populist base…but he has to gain political allies from outside that base. His ability to gain political favors from the same folks he so often demonizes is going to be tougher that he thinks.

Wildcard: IF GOP and moderate Dem politicians think that voters are getting tired of the daily “crazy” from Trump White House aka Reality Show...they will move away him and his policies. Voters from coastal and urban regions/cities in general outnumber Trump voters from Red County America 63% to 37%. IF the #Resist movement gains as much traction as the 2010 Tea Party, allegiances will get messy.

Action To Take:Not ready to Protect Portfolio Value from Further Retracement…Yet. So far all the major averages have held key support. With Apple and AMD among others announcing earnings today we are about to get attention BACK to Q4 earnings and first half guidance. 75% of (almost 250 companies) have exceeded guidance and estimates…that is a very good indicator of Q4 strength.

Tech heavy Nasdaq Comp is similarly healthy and intact as is the “America First” Russell 2000 Small Cap index which got wildly overbought in the TrumpTrade euphoria. It actually is the least strong chart as its right at key 50-day moving average support.

Political Update

Tax cuts are almost 100% certain, though their beneficiaries are not certain at all. Constitutionally, all tax bills must originate in the House, and their impact on the deficit will be important to any traditional fiscal conservative House Republicans. Passing a tax cut may depend on having a corresponding set of spending cuts ready. Fixing taxes could be problematic: Every dollar the government now spends (or gives in tax benefits) helps somebody, and whoever it is almost certainly has lobbyists on retainer.

The hard part is getting agreement on the big items like taxes and healthcare reform. I love seeing Trump and Pence and Ryan and McConnell and all the guys holding hands and acting as if they’re all ready to walk into the bright new future together, but the reality is that there are some quite different ideas in Washington about what serious reforms should look like, and a lot of congressmen want to put their personal stamp on the final bills.

The Dodd/Frank reform effort that Wall Street has bought into could also fall apart for various reasons. The Senate majority is narrow enough that just a handful of GOP defectors will be able to stop any given bill, assuming Democrats stay united in opposition. Republicans better be on guard against hubris IMHO.

Finally, as always there is always the chance that some “bolt from the blue” could change everything. An international crisis, a large bank failure, terror attacks – any one of a long list of unforeseeable events could conceivably derail this train. We will also see votes for populists in France, Netherlands and Italy by summer and the final form of the U.K. Brexit from the EU this Spring.

Key point: IF we through the first 100-150 days with this administration, then I think its agenda will have enough momentum to keep rolling.

Assuming no major surprises, I think the tax and regulation changes can boost GDP growth in the final half of 2017 toward the 2½ percent range. That will be a small improvement from this year and could set the table for a bigger feast in 2018 and beyond if the Trumponomic agenda passes intact.

Much also depends on how the Federal Reserve responds, as well as on any changes in its composition. I assume Trump with appoint Fed members who are “dovish” aka want rates to move slowly. THAT lack of action will but a floor under that stock market

Really Key Point: The biggest risk in U.S. stocks is that many stocks already HAVE 15-20% corporate tax rates baked in now. To see what’s at stake in the U.S. equity market look no further than the torrid performance of companies perceived as benefiting most from corporate tax reduction.

Featuring companies ranging from CME Group Inc. to Gap Inc., the group has returned almost double the S&P 500 Index since the election and added $79 billion in value, according to a 49-stock basket maintained by Goldman Sachs Group Inc. The index, which includes companies with the highest tax rates, is coming off its biggest rally relative to the equity benchmark since 2013.

The bulls who have piled into the heavily levied group will now be looking for confirmation the new president will deliver on his proposal to lower the corporate tax rate to 15 percent from 35 percent. The same waiting game has been playing out in a variety of sectors since Election Day as everything from banks to oil drillers have seen once-blistering rallies flatten out in the January 2017.

IF the Republicans get all timid or can’t cooperate and end up settling for the usual tinkering around the edges with tax reform and healthcare reform; and if they are stymied by an entrenched bureaucracy that doesn’t want to see its regulatory powers dismembered, then we can’t expect to get the economic boost that everybody is anticipating. If a policy-driven boost doesn’t materialize, the markets, which have jumped on the anticipation of Real Change, will reverse just as quickly.

“The market will do whatever it takes to cause the most pain to the most number of people,” was the litany he repeated to me, over and over when I started on Wall Street with what turned into Kidder Peabody. I never forget those words..

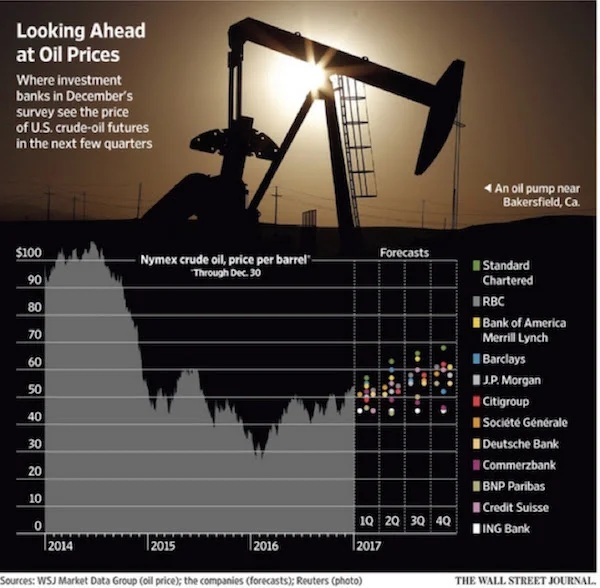

Energy Outlook: More Drilling/Production than EVER

Energy stocks have been tearing higher since the election on bets that the Trump administration will relax environmental restrictions and open more federal lands to oil and gas drilling. Crude oil’s staying north of $50 hasn’t hurt, either. It is up there in part because OPEC obviously threw in the towel and agreed to production limits.

Unfortunately for OPEC, those limits don’t apply to US and Canadian shale producers. And the history of OPEC is of course that they all cheat like crazy on production limits.

My friend Art Cashin from UBS has an internal “friends and family” list to which he generally sends one or two short, pithy notes per day. For quite some time now, he has been noting the high correlation between the price of oil and the stock market. That correlation is why I have moved my thoughts on energy into our January 2017 newsetter Part II. The price of energy is important to our portfolios in ways that are not clearly understood but can be observed.

It would require a perfect storm of events to get oil to $60 and stay there IMHO. The main reason is with the U.S. shale frackers now the swing players in oil production, there are BIG technology moves coming quickly into shale production.

Key Point: We are about to start a new oil patch pattern: Production should keep rising even as prices fall. Conventional wisdom says that producers stop pumping at some point when it becomes unprofitable, but I think that is about to change.

If you are an oil producer – or really, any commodity producer – two things can improve your profit margin: higher selling prices for the resource you produce, or lower production costs. Some combination of both works as well.

Selling prices are mostly outside the producer’s control, though adept hedging can help. Cost reduction is therefore the place to concentrate your attention. The automation of shale drilling is happening a LOT faster than you hear about. Many oil services drilling and fracking outfits are projecting they can drill and frack shale wells with 50 to 75% LESS humans.

Rigs have gotten so much more efficient that the shale industry can use about half as many as it did at the height of the boom in 2014 to suck the same amount of oil out of the ground, says Angie Sedita, an analyst at UBS Corp. Nabors Industries, the world’s largest onshore driller, says it expects to cut the number of workers at each well site eventually to about FIVE from 20 by deploying more automated drilling rigs.

Key Point: There are significant chunks of the petroleum-producing parts of the United States where $40 oil will not be a barrier to drilling and new production. Eventually – in a few years – these techniques will begin to show up in wells around the world, and there will be an explosion of oil.

If Trump permits construction of more pipelines and natural gas export terminals, we could see North American exports rise considerably in the next few years but NOT oil prices. IF we engage in a full trade war with Mexico, the 6-8% of natural gas produced in America and shipped to Mexico (mostly by pipeline and some by LNG ship) will stay in the U.S. and hurt nat gas prices 30-40% with oversupply.

Update on China

This is going to be a pivotal year for China. Having to deal with a US president who refuses to play by Beijing’s rules is only part of it, and not necessarily the most important part. China has defied gravity in more ways than I can count. We will see if it can levitate another year or whether it falls back to Earth in 2017. My base case is that they continue the levitation act, but we are going to see an increase in volatility.

I’m not sure how many people are aware that the overnight rate for offshore yuan reached an incredible 105% at one point last week. The Chinese created a massive short squeeze, trying to maintain the value of the yuan. They have spent hundreds of billions of dollars in that effort and are likely to spend more this year.

Key Point: the natural direction for the yuan, if it were allowed to float, would be significantly lower against the US dollar than it is today. The Chinese are manipulating their currency, but they are manipulating it to maintain its current value and allow it to slowly fall to its natural rate. Any precipitous move in the yuan will unsettle markets quickly like they did in August 2015.

The Chinese Communist Party will hold its 19th party congress in the fall and will almost certainly give Xi Jinping another five years at the helm. He has become China’s most powerful leader since Deng Xiaoping and could well surpass even Mao before he departs.

Xi’s government is doing all it can to keep the masses happy, mostly by handing out generous benefits and subsidies to the usual suspects, including state-owned enterprises. This help makes it very hard to tell which of China’s many state-owned enterprises are actually turning a profit vs. operating at a loss because officials have ordered them to. That is why state ownership is problematic, of course, but for China the alternative may be worse.

A major side effect is that all the stimulus sloshing through an economy with few international exits has nowhere to go. The Chinese have fairly serious limits on the amount of money that individuals can take offshore in a given year. That means there is a lot of money in China looking for a home.

The results are predictable: asset bubbles rolling through regions and asset classes whose valuations follow no discernable logic. These imbalances can’t continue indefinitely, but I don’t know how the Chinese will arrest them. The direct route would be a currency revaluation.

Xi’s hands are tied: Propping up the value of the yuan is going to force him to use his dollar reserves or to raise interest rates in an already volatile market. The Chinese are getting to a place where manipulation will be a lot more difficult than it has been in the past.

China is trying to do something that would be hard no matter who is in charge. The US is the world’s largest economy because we create most of our own supply and demand. It took us many decades to reach that point; China is trying to do it in about two decades. Their export-heavy model can’t work much longer, but they don’t yet have a way to create sustainable internal demand.

Key Point: The Chinese have been doing things that nobody thought they could do for quite a few decades now. With their National Congress this fall I expect another rabbit out of the hat. That said, all the bad conditions are in place for major problems in China. That 6.5% GDP growth rate, even if it’s close to correct (and I don’t believe it is), can’t go on forever. I don’t see many opportunities in China stocks.

The Impending European Disunion

Our fifty states are essentially what the European Union’s founders wanted: a giant free-trade zone with a currency union and fiscal union. It’s working for us in part because our states, while unique, don’t have the centuries of cultural and linguistic diversity that Europe’s do. I think we underestimate how important our common language and heritage have been to our economic development.

The separate languages, cultures, and histories of its nations don’t mean Europe can’t develop better ways cooperate economically; but the EU structure, specifically the European Monetary Union and the euro, clearly isn’t the answer. I think 2017 will make this fact increasingly obvious to everyone – and possibly undeniable if the worst happens in Italy. Let’s start there.

Italy’s banks are holding something like €350–400 billion in nonperforming loans. The vast majority of that amount is not just temporarily non-performing loans; it’s dead money, up in smoke and off to money heaven. The banks are pretending otherwise, and the government is letting them. So is the ECB. This is a fact Europe must face. Yet no one wants to face it, and so the leadership is trying to pull off an increasingly ludicrous shell game.

We forget sometimes that banks are themselves borrowers. Most of their lending capital is not equity. They get it by taking deposits and issuing bonds. If a bank can’t collect on the loans it made, it can’t repay the money it has borrowed, and the whole edifice collapses. Bank collapse is ugly, and minimizing the ugliness is one reason we have central banks. We expect our central bankers to remain sober even while everyone else imbibes.

The European Central Bank may be sober, but I’ll bet more that than a few of its member countries would like a drink. Especially in Italy. They are in a near-impossible situation. Huge imbalances exist within the Eurozone with no mechanism to resolve them, and Italy is one of the southern-tier countries that is bearing the brunt of the refugee crisis. That’s not the ECB’s fault. The system was never going to work. Now people are realizing it’s broken, and they are fighting to get out with what they can.

Inflation last month finally reached 1.7% in Germany. You can bet the drumbeat for tighter monetary policy, in place of the all-out massive quantitative easing that we are currently seeing, is going to grow louder in Germany and most of the other northern countries. That is exactly the opposite of what Italy and the southern countries need. See the potential for conflict?

Last week I saw a Spectator article that was not encouraging. I can’t say the following any better than the writer, James Forsythe, did, so I will just quote him.

- After the tumult of 2016, Europe could do with a year of calm. It won’t get one. Elections are to be held in four of the six founder members of the European project, and populist Eurosceptic forces are on the march in each one. There will be at least one regime change: François Hollande has accepted that he is too unpopular to run again as French president, and it will be a surprise if he is the only European leader to go. Others might cling on but find their grip on power weakened by populist success.

- The specter of the financial crash still haunts European politics. Money was printed and banks were saved, but the recovery was marked by a great stagnation in living standards, which has led to alienation, dismay and anger. Donald Trump would not have been able to win the Republican nomination, let alone the presidency, without that rage – and the conditions that created Trump’s victory are, if anything, even stronger in Europe.

- European voters who looked to the state for protection after the crash soon discovered the helplessness of governments which had ceded control over vast swathes of economic policy to the EU. The second great shock, the wave of global immigration, is also a thornier subject in the EU because nearly all of its members surrendered control over their borders when they signed the Schengen agreement. Those unhappy at this situation often have only new, populist parties to turn to. So most European elections come down to a battle between insurgents and defenders of the existing order.

As James Forsythe says, the conditions that won Donald Trump the presidency exist in Europe as well and are possibly even stronger there. They manifest differently under parliamentary systems, but I see no chance that they will go away. They’re getting stronger, and I think we’ll see proof when France, the Netherlands, and Germany hold national elections this year. It is likely that the Italians will also have to hold snap elections because of the banking crisis, and it is not entirely clear that a majority would support a referendum on remaining in the euro (which is different from remaining in the European Union).

The anti-EU, anti-immigration parties may not win outright control in any of the four countries, but they can still exert enormous influence. These parties may not have the solutions, but the incumbents definitely don’t have them. Given a choice between unlikely and impossible, you have to go with unlikely. That’s what Europeans are doing.

I expect 2017 to bring many changes to Europe, but I’m not convinced it will be the end just yet. “Delay and distract” has worked well for the pro-EU, pro-euro forces ever since the sovereign debt crisis hit in 2010. The europhiles are true believers who simply won’t give up. At some point their determination may not matter, but I suspect they can keep doggedly kicking the can down the road until 2018 or later. It is just not clear when they will run out of road.

When they do, the result will likely be a very severe recession in Europe, which will embroil the world and could push the US into recession if it happens too quickly. Perhaps if we muster the reforms we need here in the US and actually get some sustainable growth going, then a fragmenting Europe might just knock that growth back to the sub-2% or even sub-1% range. But if China, too, loses the narrative in 2017, then all bets are off.

A Few Final Thoughts on 2017

Of course "Make America Great Again" is shorthand for bringing back 3-5 million jobs lost to Rust Belt voters in manufacturing. Well the US is manufacturing more materials and goods than ever. If fact manufacturing is increasing at a fairly serious rate, well over 2% a year for the last decade.

The problem is, those promised manufacturing jobs are not. A Ball State University study calculated that it would take more than 8 million additional jobs to produce what we currently produce today if we were merely at the productivity levels of 15 years ago. From 1980 it took 25 workers to produce $1 million of goods (inflation adjusted)...today it takes 5 workers.

Investment in automation and software has doubled the output per U.S. manufacturing worker over the past two decades. Robots are replacing workers, regardless of trade, at an accelerating pace..and even in the oil patch we can forecast 2 roughnecks to frack a well that used to take 10 roughnecks. “The real robotics revolution is ready to begin” writes BCG and predicts that “the share of tasks that are performed by robots will rise from a global average of around 10% across all manufacturing industries today to around 25% by 2025.” (Source: fortune.com/2016/11/08/china-automation-jobs/)

Key Point: Here is the Economic Conundrum: IF we don’t automate faster, we lose jobs by being uncompetitive. If we do automate, then we see jobs go away. What we have to do is figure out how to make sure that new jobs are created, and that these jobs are simply not make-work but are rather meaningful and fulfilling.

As an economic matter, lower costs and higher productivity are deflationary. Excess supply in the absence of higher demand pushes prices downward. This is why we’ve seen such sluggish growth in the last decade. At some point, faltering growth may turn into outright contraction on a global scale. Then the real problems will begin.

Politically...the promise to bring back manual labor based manufacturing jobs is a mirage...they can't come back because they no longer exist.

This is the macro-risk with Trumponomics: there is no way to pay off his manufacturing jobs promises.

Then what?

Well thankfully that reality is way down the road.

Cheers.

- Toby

Copyright © 2017 Transformity Media, Inc., All rights reserved.