September 2017 Newsletter

Welcome to the September Transformity Investor newsletter edition. Our team will go over ALL our positions, targets and buy under prices and quickly (really!) get an October newsletter our heavy on charts. A suggestion by a new subcriber to "put the stocks/ETFs that are under your buy under price in bright green!" has been executed!

Note on the new website transformityresearch.com: We have had a few folks who could not process their new subscription. In every case the problem was your password. Like all modern web sites, your password MUST NOT be "ZZZZZZ" or 1111111 ok? It should not be derivative of your email address either.

Use a password that has 6 or more letters and numbers...you will have no problem registering. Go to www.transformityresearch.com and click on the "Members" tab on the top right hand of your browser screen.

For those who missed our announcement last week: In order continue your service we need you to subscribe to our new server and payment system with a new one-year subscription of $97. We will then add your remaining months from your current subscription to your new subscription.

Simply click on www.transformityresearch.com and click on the "Members" tab in the upper right corner of your browser. Click on the one-year $97 button and register for our new service (which includes FULL website access!!!).

Why the hassle? Ah, publishing technology. Our old system will not transfer to the new system is the short answer. Also...there are a NUMBER of subscribers (as in >100) we found in this transition who open and read our newsletters and updates but are not currently paid subscribers (and you know who you are!).

In order to have a fresh start, and to "encourage" those who have been benefiting from our 6-to-1 outperformance of the overall stock market with our portfolio buys/holds and sell advice, we wanted to give ALL of you a 3 week transition period.

After October 15 we will scrub our subscriber list and ANY unpaid subscriptions will be terminated.

Why should you continue our #1 rated investment newsletter? Silly--our ind-blowing performance is why.

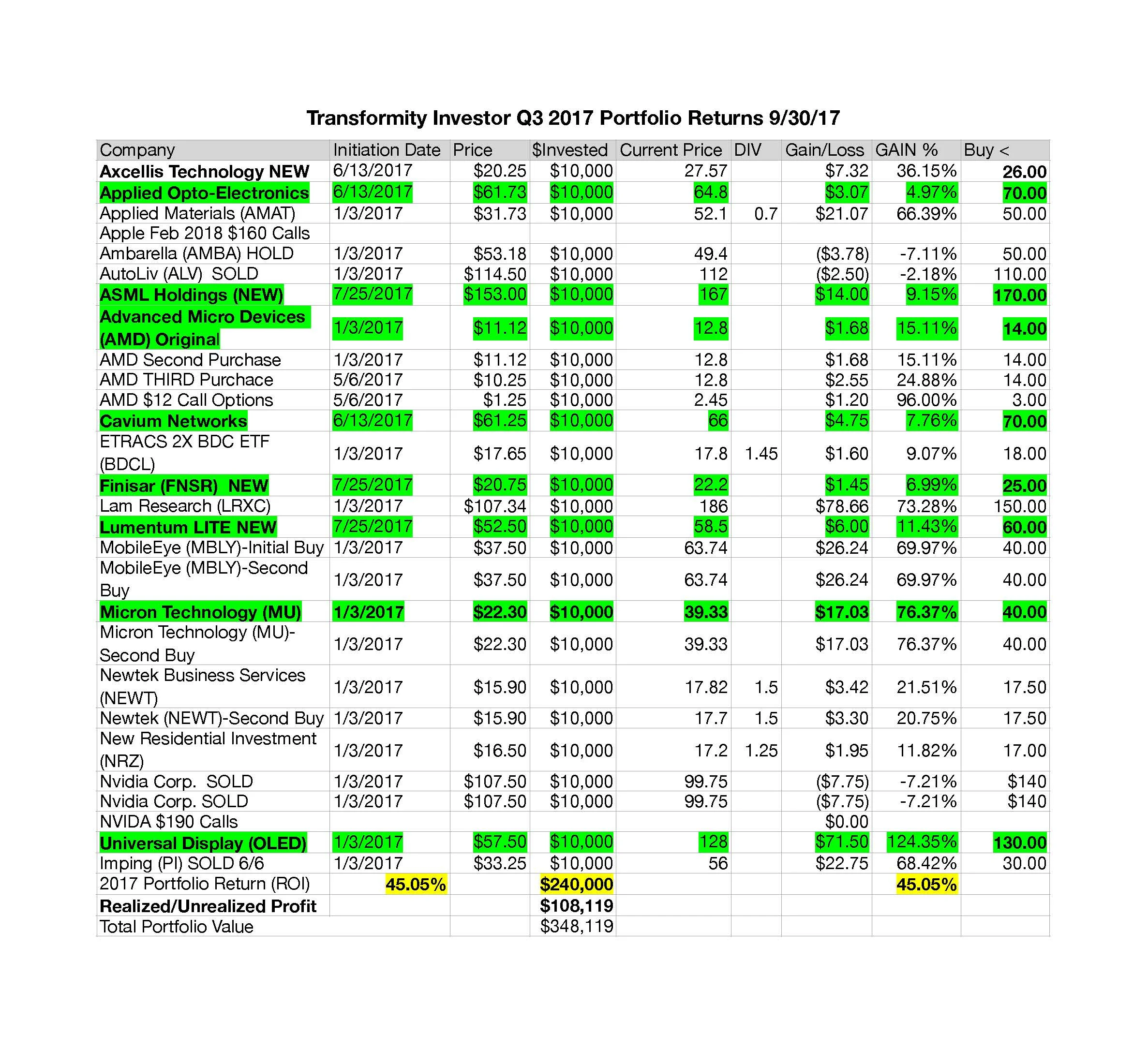

For the last 21 months our portfolio of $10,000 investments in each of our 27 stocks, ETFs and long-term options from 2016-2017 recommendations has increased over $324,000 in value or 120.1% vs. S&P 500 performance of 15.7%--nearly 800% outperformance over passive index investing and 2000% of 20 TIMES the average hedge fund return 5.2%

Our 2017 Performance is now 45% vs. just 11.2% for the S&P 500

Again...Simply click on www.transformityresearch.com and go to the "Members" tab on the top right-hand corner of our site, click on the one-year $97 button and register for our new service (which includes FULL website access!!!).

IF YOU HAVE ANY PROBLEM...just call or text Majorie Smith 10-6 PST at (301) 520-9610

AGAIN...if you have been receiving and opening our paid service and are NOT CURRENTLY a paid subscriber--I have the list in front of me and it's pretty long...do the honorable thing and subscribe to our service or your unpaid subscription will end in the next 14 days. No hard feelings...just do the right thing!

September Newsletter: The 4 Quarter Market Melt-Up Is Coming

#1 3rd quarter growth for the US Economy is going to be slower--our main GDP forecasting index from the Atlanta Fed has come way down from 4% to 2%...so we DO need to be on our toes and use our Transformity MacroMarket Index to let us know when a recession in 4-6 months away and that we need to KEEP OUR PROFITS.

Transformity MacroMarket Index: 16.8--ALL CLEAR to own stocks for the next 6 months.

I continue to make the same forecast on the US economy: IF we get real tax reform then the economy and the stock market is back in the hands of the Federal Reserve. Despite 5 YEARS of below 2% inflation (note to new subscribers: Go to the website www.transformityresearch.com and look at the last 3 months newsletters to get the analysis and assumptions we use to come up with the following forecast), there is 100% correlation between the Fed raising short-term rates too high and recessions 17 months later.

I still think (based on all the economic data we get--45 indexes) that mid-2019 is where the market risk is where at the margin a 2.5-3% 10-year bond sort term Fed Funds rates get above 1.36%

Why is 1.36% important? Because going back six decades we (and others) have found that WHEN the fed-funds rate exceeds the 10-year cyclical low, on average a recession follows within 17 months. Call this the "recession early warning system." Now, what is DIFFERENT this time, of course, is persistently low PCE inflation rates and equally low productivity rates (output per hour of labor). IF we get new Fed Chair and the 4 new appointees are NOT inflation hawks fighting the Phillips Curve battle (the economics "law" that says under 5% unemployment causes wage inflation that kicks off an inflation rise) then I'd discount an over-active Fed.

Key Point: The market now projects 80% change of 25 basis point rise in the Fed Funds target in December...THAT would take the Fed Funds rate OVER the 1.36% cyclical 10-year bond low...just saying. 17 months would take us into the first quarter of 2019--bear markets start 4-6 month AHEAD of recessions.

Really Key Point: Our best judgment today is we have 15-17 months of runway LEFT to add another 60-80% of profits to your portfolios.

So Ladies & Gents: the two big questions in the market are as follows:

- What are the REAL odds of getting REAL tax reform done in 2017?

- With so many HUGE hedge funds down for the year and the entire hedge fund performance at a PATHETIC 3.1% in a 11.1% S&P 500 (that is AFTER FEES of course), what are they going to bet on to attempt to salvage their year (or they are going to have a LOT of money taken away from them).

Addressing question #2 first, we got a preview of what some kind of end-of-year rotation to lagging financial and energy might look like this month. After eight months of tech and to a much less degree healthcare dominance, the record-breaking S&P 500 has assumed a fresh new face in September, being instead led higher by energy and telecom shares.

Digging deeper, as the scorching-hot FAANG stocks — Apple, Facebook, Amazon, Netflix and Google — have headed toward correction territory this month, energy producers have stepped up and largely filled the void, aided by a surge in crude oil prices (but we are NOT going to chase them).

The Good News: The resilience shown by the S&P 500, which just last week hit a series of new record highs, goes a long way towards disproving the notion that the stock market is trading at the whim of the just the tech industry. That's good news for bulls and a comeuppance of sorts for skeptics that warned against a market reckoning in the event of tech weakness.

Better News: Our 2-3 year secular transformational growth Super Sectors are growing their eanrings at 10-50X faster than the overall economy. Our favored secular transformation Super Sectors?

5) Autonomous Driving 6) 40-G to 100GHyper Data Centers and 7) Transformation from 4G to 5G Wireless.

You can add rising short term and long term interest rates IF we get the expected Fed rate hike in December.

And yes our IP Leaders in our favored secular transformational growth sectors are KILLING the overall market by 4X or 400%--45.1% vs. 11.2% for S&P 500. In a 2.2% ish growth economy, compaines with non-cyclical aka secular growth selling at BELOW market valuations KILL IT...and that is most of our portfolio of stocks.

For instance, shares of our favorite OLED chip equipment makers Applied Materials Inc. AMAT, +6.36% surged Wednesday on positive momentum in the chip sector and the chip materials company's long-term forecast and share buyback program. Applied Materials shares rallied 6.9% to $51.09, helped in part by Micron Technology Inc. strong forecast for memory chips, and are up 62% year to date.

Applied Materials now forecasts forecast adjusted earnings of $5.08 a share in fiscal 2020 as Internet-of-things applications, Big Data and artificial intelligence drive computing demand. For the current year, analysts surveyed by FactSet expect fiscal earnings of $3.21 a share. The company also announced a new $3 billion share repurchase program in addition to the $995 million that remains on an earlier program.

Key Point: put a 14 p/e on AMAT and it's a $90 stock. ALL the secular trends we love require new advanced materials to work--AMAT is in the sweet spot. Axcellis ACLS is a mini-AMAT...which I believe gets acquired by Lam Research or KLAC in 2018!! We will add KLA-Tencor (KLAC) on next pull back.

The rotation occurring underneath the surface of the S&P 500 this month — out of tech and into other more attractively-priced areas — has played out on a smaller scale a few times in the past several months. On multiple occasions, exchange-traded fund data has supported the idea that money pulled from tech has simply been reallocated elsewhere in the stock market, keeping indexes afloat.

Key Point: This is we CHERRY PICK the best sectors and best IP owners in those sectors ok? “Tech” is now 31% of the S&P 500 but it is NOT a single group and valuation. This dynamic has also been in play outside the confines of sectors. Looking strictly on a return basis, the top 20% of stocks in the S&P 500 in 2017 through August have evolved into the worst-performing quintile in September. On the flip side, the bottom 20% from the first eight months of the year is now the top quintile this month.

Speaking of Cherry Picking—how about Micron?

Micron has been my favorite play on DRAM and 3D NAND price increase wave since 2016…and BOY has it made us all a LOT of money.

The good news? I’m upping target to $50 and 9 p/e because every year our consumer and industrial digitalia aka everything…cars, phones, iPads, AI data centers, door bells, laptops, PCs, gaming consoles, 4K TVs…uses more and more DRAM and NAND memory.

Action to Take: We will buy June 2018 $40 Call Options When it pulls back under $36-$37

In some regards there’s almost too much of a bullish consensus on Micron Technology, Inc. (NASDAQ:MU), In fact, a handful of analysts all but made sure of this, recently, speaking fondly of MU and, in some cases, upgrading Micron Technology shares. Here’s a closer look at the most recent wave of over-the-top optimism.

To be fair, much of the recent praise for Micron is well deserved. The company just logged four straight quarters of revenue growth, as well as four straight quarters of sales growth. Some of that progress has to be attributed to rising DRAM (memory chip) prices, though a big chunk of it has to be chalked up to the fact that Micron just knows how to make and market a great product at the right time.

That’s the way Susquehanna analyst Mehdi Hosseini sees it anyway, as he recently upped his price target on MU stock from $40 per share to $50 (it’s currently trading around $36, for perspective). “All in all, we expect [the] stock to move towards our updated PT of $50, driven by prospects of higher normalized earnings, and continued re-rating,” he wrote. If this was just Susquehanna’s take, it might not even be worth mentioning; it’s not just Susquehanna, though.

Evercore ISI recently mirrored Susquehanna by upping its target price on MU stock from $40 to $50 as well, noting, “Yes, this time is different” (in reference to previous memory pricing booms that have gone bust all too quickly).

Key Point: The last mass exodus from the memory-making market, prompted by the then-glut, has left only three major DRAM players supplying the entire market; SK Hynix (OTCMKTS:HXSCL) and Samsung Electronics (OTCMKTS:SSNLF) are the other two. There’s still more than enough business for each company, though, as the barriers to entry for the DRAM memory business are relatively high — high enough for Evercore ISI analyst C.J. Muse to suggest DRAM supplies will remain tight even though companies have already planned between 15% and 20% more capital expenditures on DRAM for next year.

BUT...It’s Goldman Sachs’ teh MU hater now new-found love of Micron Technology, however, that puts the exclamation point on this spat of optimism. Goldman analyst Mark Delaney recently reversed his May downgrade of MU stock, calling it a “Buy” again earlier this month.

“While we believe it could be the mid- to later stages of the memory upturn and note memory fundamentals can change quickly, our industry discussions suggest 4QCY17 DRAM [dynamic random-access memory] pricing could rise (with NAND [flash memory] flat to up) and the DRAM cycle could remain tight in 2018.”

Delaney added he thinks DRAM prices could rise another 10% in the second half of this year as memory chip companies further penetrate the server market. This year’s total capital expenditures on DRAM should be up 24%, according to the Goldman analyst.

And here’s the interesting part about the recent comments and upgrades from analysts: The three upgrades and upped price targets discussed above still don’t reflect the majority opinion, leaving the door open to even more price-lifting upgrades in the near future.

Bottom Line for MU Stock

As of the most recent look, the analyst community feels MU shares are worth $44.28 per share; Evercore and Susquehanna are both saying $50. That average target is apt to rise once more analysts follow the lead of those firms, as well as Goldman.

Our call is the upper-end target price of $50, MU’s 2017 P/E ratio is still a dirt-cheap 10.6.

IF you own ONE stock for the rest of the year...make it Micron AFTER it pulls back under $36-$37. We will buy a double dose of long-term $45 June 2018 and January 2019 call options on the pull back.

Really Key Point: If I am a hedge fund I am desperate right now with such wicked under-performance. IF I can buy secular growth stocks at VALUE prices (like MU AMAT ACLS LRCXKLAC) I get my cake and eat it too. When AMAT told analysts this week they forecast $5.20 EPS and are rebuying $3 BILLION in shares, that gives MU, AMAT LRCX KLAC (which we will add to on next pull back) a total green light.

The Biggest Risk to the Market: Those Investors Who Believe 2017 Tax Reform Bill Will Pass As Advertised

You would think by now intelligent investors understood the circular firing squad that is the Republican Party. But judged on the last run of stocks (btw—I was out of the country in Italy for 12 days if you follow me on my Facebook page—and when I leave the country the market ALWAYS goes up!)…it appears to me they are still living in the same delusionary world as their shameless clueless leader.

On Wednesday President Trump read a teleprompter speech promising “the greatest tax reform in the history of the world.” It will be “terrific” and create “3-4% growth again just like the glory days of late 90’s--maybe 6%!" Small business will go on a hiring binge sucking up millions of unskilled mostly unemployables and pay the middle-classs wages for jobs that do not exist in 2017 just like the good old days.

This will all sound snazzy except for one thing; this delusion is 100% destined to fail as advertized. YES passing tax reform IS an existential event for the traditional GOP...they will get killed in 2018 if they don't. It will pass purely to avoid political armegeddon.

Read my lips: anyone thinking that tax reform is a slam dunk should quit drinking the #MAGA kool-aid and think like an adult and star-struck struck teenager.

How do I know this? For one these are the same politicians who bragged and promised that repealing Obamacare would be a breeze, and how’d that work out? They, or at least Trump, also peddled another kind of snake oil, namely that tax reform would also be a cakewalk. We’re eight months into the Trump era now and that cakewalk is about as likely to happen as Trump beating Steph Curry in a game of horse on the White House basketball court.

For investors, here’s the real question: Why on earth should anyone believe anything that Trump, McConnell and Ryan have to say anyway? They run both ends of Pennsylvania Avenue and haven’t passed one major piece of legislation—not one, including what will be another embarrassing flop on Obamacare this week.

Yet the market, still surging, has clearly priced in tax reform like it’s a done deal.

THIS is my biggest worry in the markets right now. We are entering into earnings season and we KNOW on year-over-year basis earnings growth will be 10%+ for the S&P 500 and 20%+ for the Transformity Investor stocks. A retroactive 2017 tax cut WOULD MAKE stocks with earnings more valuable...espcailly ones that pay over 20% effective rate.

The problem is that EVERY 1% of tax rate cuts costs about $100 billion over ten year reconciliation period and this fairy tale dreaming outload was dismissed by his own aides several weeks ago. Trump wants one thing, GOP leaders on the Hill something else. To switch metaphors, this IS the proverbial gang that can’t shoot straight.

The reality here? It took Reagan 6.5 YEARS to get to major tax reform and that was in an era of bi-partisan legislators and no hyper-partisan media on 24/7 (read Fox News and MSNBC). The reality is the very nature of tax reform itself renders the whole cakewalk argument bogus and anyone with half a brain knows this. On an individual basis, overhauling the tax code, fiddling with rates and income thresholds means there will be winners who will pay less—but losers who will pay more.

Check out my full analysis here: How Stupid Does the GOP Think We Are?

Since 20% of Americans at the top pay 95% of income taxes, the top 20% aka “entitled elites” will get 80-90% of the tax benefits ( we need to see the tax brackets by income level.) That reality (and the fact the Gary Cohn could not sell ice to someone in Puerto Rico--his performance in selling "tax reform" has bee ludicrously bad--yo Gary can you hook me up with a $1000 full kitchen remodler?)

This is why Democratic leaders like Senate Minority Leader Chuck Schumer have such big smiles on their faces these days. They know that tax reform—like a thousand-piece jigsaw puzzle—will take a long time to put together and will soon have a BIG seat at the table. Naturally, they’ll bring different priorities to that table. They’ll oppose Republican efforts to slash taxes for the wealthy. They’ll back policies that benefit the middle and lower-class. Tax rates, income thresholds, deductions for this and that: it’s a messy, complex process. FACT: IF you think trying to do something about healthcare is messy, this is worse.

Reality is a Bitch in DC

Between the lines: Many Republicans will tell you the party is better at taxes than health care. That is bullshit.

Consider this: These are the tough hard decisions Congress already has to make in order to pull off tax reform:

- The Senate Budget Committee has to pass a budget, which is likely to allow as much as $1.5 trillion to be added to the deficit through tax reform (not accounting for economic growth). Conservative deficit hawks have to completely reverse their "strongly held belief systems" and fold.

- Graham and Ron Johnson, who are on the tax reform committee, have indicated they won't vote for a budget that doesn't pave the way for healthcare as well. (Though it's unclear whether Graham will still take a hard line on that after his comments yesterday.) If they hold out...which I don't think they will, there are only 32 legislating days LEFT in this Congress.

- The Senate as a whole has to pass a budget, which will probably come with the same disagreements as in committee, except among more members. Republicans can only lose two votes. Corker is leaving, McCain is cranky and losing one more vote kills tax reform in 2017.

- The House and the Senate then have to agree on a budget. The House budget includes instructions for $200 billion in deficit reduction — so somehow that has to be merged with a Senate budget that would allow $1.5 trillion to be added to the deficit.

- The six states with the highest tax rates are CA NY NJ IL CT MA ...eliminating the state and local tax deductions are going to be a BRUTAL fight with both Dems and Moderate GOP Senators running in 2018. But the bill does NOT work without the $1.2 trillion in new revenues...so at the end of the day GOP will HAVE to vote 52 votes in the Senate for the bill and suck it up or NO BILL and certain death.

- Then, after all of that is worked out, that's when they get to fight over actual tax policy.]

- Again...they have 32 legislative days LEFT untill Congress term is over.

Our thought bubble: A party made desperate by its failure to pull off a key campaign promise is about to step into another major legislative food fight they HAVE to pass. Political death sharpens the mind and softens the spine: Our forecast is it DOES pass and some index is applied to high tax states.

Everyone HATES the Stock Market…YEA!!!

More than 80% of chief financial officers surveyed by accounting firm Deloitte said U.S. stock markets are overvalued, marking the highest level since Deloitte began conducting its quarterly poll about eight years ago.

Overvalued markets are worrying CFOs...awesome!

The Dow has rung up 42 all-time highs in 2017, the S&P 500 index has booked 37 records, while the Nasdaq has ended at a record 49 times, so far this year.

Fretting about stock-market valuations isn’t new. According to a July study by StarCapital Research, the U.S. has the least affordable equity market in the world.

MarketWatch’s Mark Hulbert warns that when stocks become elevated, it doesn’t take much to tip them over the edge into a sharp fall, with seemingly no external triggers. That’s not to mention all the genuine external tensions abounding. Those include elevated antagonism between the U.S. and North Korea, which recently threatened to detonate a hydrogen bomb in the Pacific Ocean this weekend, and a Federal Reserve attempting a historic right-sizing of its asset portfolio even as its leader has described stubbornly low levels of inflation a “mystery.”

This is awesome for stocks. As I have said ad nauseum, bull markets do NOT DIE when people hate stocks. They peak when everyone LOVES them and all the money available to buy them is used...and then money is borrowed to buy them too.

My old friend Laszlo Birinyi, who accurately forecast that the S&P 500 would hit 2,500 by September, thinks the stock market has more room to run before 2017 is over. He attributes his outlook to the belief that market enthusiasm remains pessimistic, which he thinks is a contraindicative signal. Me too.

We are climbing the proverbial “Wall of Worry.” For those unfamiliar with the Wall of Worry, it refers to the fact that the stock market best builds a sustainable rally in the face of mildly negative news. After all, irrational exuberance is the hallmark of a bubble and fiercely negative news is the sign of a crisis.

Thus, the more we wring our hands and nitpick the little things, the more justified this double-digit run for the S&P 500 SPX, -0.22% since Jan. 1 becomes. Such negativity keeps the bull market honest, or so the thinking goes. I LOVE that high profile worriers abound — from Jim Rogers and Robert Shiller last week to previous warnings from billionaires like Jeff Gundlach, Carl Icahn and Warren Buffett, just to name a few.

Here is economic reality.

Businesses see great earnings: Why shouldn’t the U.S. stock market be at records when corporate earnings are near records themselves? The blended growth rate for the S&P 500 in the first quarter was 14.0%, according to research firm FactSet, and the best since 2011. While year-over-year growth slowed to “only” 10% in the second quarter, stocks simply obliterated expectations with 73% of S&P 500 components topping earnings targets and 70% beating on sales. Yes, the pace of earning growth is set to be slower as we finish the year. But why should we think a crash is around the corner when the rally has been built on real profits and not just rosy sentiment

Consumer metrics are strong: It’s no secret as to why businesses are prospering. U.S. unemployment is around a 15-year low and consumer confidence recently hit its highest level in nearly 17 years. The housing market continues to show resilience, adding to the “wealth affect” and optimism in middle-class households. As we approach the all-important fourth quarter when holiday shopping and consumer spending can pack the biggest punch, the state of play looks pretty darn good for consumers.

Global resilience: Beyond the U.S., look at the favorable growth metrics in every corner of the globe. The OECD recently projected global growth will increase to 3.5% in 2017 from 3.0% in 2016 — and accelerate to 3.7% next year. Separately, the IMF increased its outlook in spring to 3.5% growth this year and 3.6% next year and recently reaffirmed those targets. Sure, North Korea is talking crazy again. But similar localized geopolitical problems, such as the brutality of ISIS in Syria, have been persistent for years and haven’t caused major disruptions. Let’s not start panicking now.

Doomsday metrics are often wrong: Folks love to post charts “proving” the market is doomed. But before you freak out about the data du jour, keep in mind that many of these metrics have been consistently inferior indicators of market trends since 2009, if not longer. Take Robert Shiller, who once again made a splash pointing to CAPE readings that appear bearish. Except he did the same thing over two years ago and stocks have had no trouble moving higher. And more importantly, in previous bearish commentary he admitted CAPE — the cyclically adjusted price-to-earnings ratio — could be an unreliable indicator of where we’re headed. “This stock market is an enigma,” Shiller said. “While history suggests current levels signal a correction, it doesn’t mean we will have one soon. CAPE could go higher, as it did in 2000.” And CAPE did go higher, from 28 to 30 over the last two years — and stocks went higher, too. Remember, plenty of data show market prognosticators are generally wrong more often than right when they have numbers to “prove” their case. Keep that in mind before you hysterically retweet a chart that shows a crash is inevitable.

Stocks are still the best game in town: More important than all of these items is the notion of “opportunity cost” for your money. After all, even if some of the negative headlines are justified… where do you plan on putting your money? Despite talk of tighter monetary policy, the 10-year TreasuryTMUBMUSD10Y, -1.61% yields well under 2.3% — less than it did late last year before the Fed’s rate increases in December, March and June. Junk bonds offer significantly more yield, but as we saw in the bloodbath of 2015, they also come with a heap of risk. Same for gold GCZ7, +1.26% which may sound like a store of value to some but burned quite a few investors as it melted down from its 2012 peak.

Key Point: If you are a money manager who is trailing the S&P 500 index BADLY you have to have a better idea than stocks if you have a hope of a job next year.

In 2017, there are not any alternatives to catch up other than stocks. We will see a melt-up of stocks into the year-end and THEN a profit-taking melee in early 2018...we will be ready and positioned!

Thanks to all who have re-upped their subscriptions to Transformity Investor--strap in and buckle up for a BIG profits as the hedge fund melt-up is coming!

- Tobin

Copyright © 2017 Transformity Media, Inc., All rights reserved.