May 2019 Newsletter Part II: Now It's Serious

We are LOWERING Risk Exposure & Raising Cash for Slow Meltdown over Next 65 Days

Dear Subscriber,

Well, it took a little longer than Tuesday (I am a perennial optimist) but we have processed a LOT more data and conversations.

I never imagined 30 years ago my investment and macroeconomic research process would be reduced to game planning $600 billion trade tariff war (inflation-adjusted 3X bigger than the Smoot Hawley tariff war the caused the world's Great Recession) and mind reading a celebrity TV reality show host POTUS as to when he or the President-for-Life of the People's Republic of China can't take the economic and political pain any longer and finally come to a real meaningful trade agreement that both leaders can sell to their legislators.

Note: did you ever play that game in a bar when you were young where a dude has a battery with two nodes attached and you hold them as he turns up the voltage? This was a right-of-passage in the '70s and '80s in Baja California. You bet your buddies you could hold on and endure the most pain as the dude cranked up the voltage diel--loser in the group bought the group another round of beer and tequila shots.

That is my analogy here: Trump holds the battery and the voltage dial. He is turning it up--slowly at first but now with bigger moves. Xi is holding the two nodes and in a machismo act he is pretending he does not feel the pain--but we know he does feel it. He's asking the VERY loyal and nationalistic Chinese middle class to "take another year-long Long March" as the did 70 years ago to take on another imperialist bully. As I will get to in a moment--unless there is a miracle settlement (which we will a way-out-of the-money call option on the QQQ and semi-conductor SMH in a bit), the next 65 days are full of risk and the only one really big risk mitigation upside is a flash settlement.

We have been through many scary and painful pullbacks and geopolitical scares. Yet with US/China global trade war escalating by the day, the prudent investor has to admit “This is new territory—making investment decisions in an expanding global trade war between the #1 and #2 economies in the 21st century has no playbook.” The Fed still has our back, but when? The LAST thing they want to do is appear to be kowtowing to Trump's tweets and insults.

Not to mention, of course, that the last trade war started by a “great businessman” POTUS Hoover in the 1930’s caused the Great Depression.

Late note: Tariffman Trump now has declared trade war on Mexico, too. Dow Jones futures along with S&P 500 futures and Nasdaq futures are tanking after President Donald Trump said he'll slap a 5% tariff on Mexican goods on June 10, saying the country is "failing to stop the flow of illegal migrants into the U.S."

Action to Take:

Enough--the Tariffman act is only getting worse and is veering out-of-control. It is clearly red meat for his Red State and "Build the Wall" base. There is NOTHING wrong with taking some profits here to build cash and stashing them in PFFA with 8% yield (which moved down .0003 at the height of the 400 point drop post-Mueller conference). I, of course, don’t know your individual portfolio—but YOU have to make the decision about a) how long term your risk investment horizon is and b) are you willing to take another 30%+ portfolio downswing in the next recession led bear market.

Action to Take:

Lower Your Risk Profile and Take The Profits on our “Dec 26 Double Down" Plays: Sell our opportunistic December buys in AMD MORL MIC NRZ BDCL that we bought in the December Flash Crash to lock in 2019 and move that cash into PFFA.

Action: BUY the QQQ July 19 $165 Put Options at $2.50 or better

My advice is this trade war gets worse before it gets better (and it has nothing to do with “rare earth” metals—more on that later). 25% or more cash in PFFA here gives you 8% ish yield (reinvested) and gives you fresh powder in the next panic “sky is falling” 10%+ correction which may happen any week.

Here is the chart that REALLY shows we are right on the edge: 2.5 Year WEEKLY S&P 500 Chart

1) On a weekly basis, we are not NEARLY oversold yet--just 52.5 RSI--a washout is 30 or below

2) We have not had a BIG down volume week yet but still, we have broken the 200-day average

3) The earnings disappointments set-up for Q2 over the next 70-80 days is profound (see below)

4) We are in the taint here--we aren't at panic sell-off fear and we are out of earnings news for 60 days.

5) Tariff headlines and earnings warnings await as the 1% ish GDP slow down gets more and more real and unambiguous

While the Fed and Central Banks have been the hero and heal for stocks since 2010, the trade wars now expanded to Mexico too are a mess. How did the steel and aluminum tariffs work out for U.S. Steel? This chart is breathtaking--brutal. $47.50 to $12 in 15 months?

Ask US Steel how effective steel tariffs work. Or Alcoa. Or

I guarantee no one is showing Tariff man these real-world results of what happens when you play the tariff card.

Obviously, Mr. Trump thinks being the tough guy on China and Mexico trade plays well with his base and the Obama voting white working class living in the 2616 counties that voted Trump in 2016. He knows their psyches better than anyone. But unless he has a secret China agreement in his pocket that he is holding as insurance or the Fed has told him "they have his back" (not at all likely) and will cut rates in their June meeting (both of which are nearly impossible to happen) here is the bear and bull case as of May 30.

The Bear Case

The bear case assumes that

1) China can take the Long March pain and is going to bet on Trump losing 2020 election while it

2) turns on the monetary spigots and devalues the yuan currency to offset the tariffs

3) the financial pain of higher consumer prices and lower agricultural prices and sales in the 2616 Trump voting counties is going to cause a revolt of the Deplorables

4) With a president-for-life, the politics favor China in a standoff with an "imperialist bully" going into the 70 year anniversary of the PRC and

5) as I have mentioned many times, China is not going to negotiate away its fundamental hybrid capitalist/mercantilist economic model and ideology to the US alone while

6) most of the G-20 thinks the US under Trumpist nationalism is undermining the G20 so China knows the US in on its own in this quest.

Reality:

Some of the biggest names in investing are bracing for a protracted superpower conflict and adjusting their portfolios accordingly. Ray Dalio of Bridgewater calls it a “long ideological war.” Mark Mobius sees little hope for a quick resolution. Mobius, for instance, is avoiding shares of Chinese exporters and buying companies that sell to domestic consumers. And longtime China investor Stephen Jen says we’re witnessing the start of a 15-round fight. “This contest will be a drawn-out process that will likely last our careers,” said Jen, a former economist at the International Monetary Fund and Morgan Stanley who now runs Eurizon SLJ Capital, a hedge fund and advisory firm. “We as investors and analysts need to pace ourselves and try to not just follow the latest news. We need to understand the economics and our vast cultural differences.”

Obviously, the bets on a base case belief that both Trump and China HAD TO settle for political reasons helped propel stocks toward record highs just four weeks ago were dead wrong. Global equities lost $4 trillion of value this month, while U.S. Treasury yields plunged to the lowest level since 2017. For Dalio, the billionaire founder of Bridgewater Associates, the conflict goes well beyond a trade war. As China emerges as a world power capable of challenging the U.S., the countries will clash in “all sorts of ways” because of different approaches to government, business, and geopolitics, he wrote in a series of posts on LinkedIn this month that didn’t mention his investments.

“They can’t negotiate these more fundamental issues,” wrote Dalio, whose firm oversees about $160 billion and has offices in Westport, Connecticut, and Shanghai.

According to the famous China investor Mark Mobius “We’re in a new game -- Trump has really opened this can of worms,” the emerging markets veteran, who left Templeton Asset Management last year to co-found Mobius Capital Partners, said in an interview with Bloomberg Television. He flagged India, South Korea, Vietnam, and Bangladesh as potential beneficiaries as the conflict spurs manufacturers to diversify away from China.

Kyle Shin of Gen2 Partners, who manages about $1.3 billion in hedge funds, returned from a recent China trip convinced that the conflict will take decades to resolve. As Chinese bonds in his portfolio mature, Shin is replacing them with high-grade corporate debt in developed markets, he said in a phone interview. The Hong Kong-based manager’s flagship fund has posted mid-single digit returns this year after gaining 20% in 2018.

Kingsmead Asset Management’s John Foo has gone even further, selling all his holdings of Chinese stocks for the first time in his two-decade career managing money in Asia. He offloaded the shares in mid-2018 because of the trade war and tightening credit conditions.

But Do Not Despair--The Bull Case IS Building: Here is What I Find the Most Compelling Reality Today

As China looks to face down Trump and is so far willing to take the short term pain, its leaders do find themselves in a real bind: How can they show him they won’t be pushed around without wrecking hope for a deal that they ultimately will have to have? Facing a slowing economy at home in China and Trump’s day-to-day unpredictability, Beijing has only at this point used one bullet--their state media to blast American policies and obliquely hint it could cut off the U.S.’s supply of rare earth metals (an alert out manana about why this threat is toothless).

Yet all this while, China been very careful not to provoke Trump further or risk worsening a rapidly deteriorating relationship. In other words, so far China’s strategy has been to not directly poke the bear. Why is that?

At the end of the day, it's the math. China knows, in the long run, it can’t afford to blow off $600 billion in annual exports and lose hundreds of $billions of capital investment in China by US companies—they get it. China’s import contraction is accelerating—down 4.5% in April and 8.5% in May. Imports from Japan down 16%—South Koran 18%—Taiwan 20%. Credit growth slowed in April and May—and major industrial inputs like cement, glass, copper and nonferrous metals as well.

“They are struggling to find sources of leverage that will hit that sweet spot of inflicting pain without rupturing ties,” said Bonnie Glaser, a China specialist at the Center for Strategic and International Studies in Washington. “‘Dou er bu po’ is still the mantra," she said, citing a Chinese phrase which means “to fight without severing relations.”

Point #1—As I pointed out in Part 1—we and others have lowered Q2 US GDP to 1% ish—that data comes out the first week of July—and Q1 revisions down as well. AFTER a 1% ish GDP print (which is after the Fed June meeting BTW), the reality of the trade war is going to show the US is not immune to the economic damage and THAT should bring Trumponomics back-to-the table.

Where We are Now

We are the middle of another rolling sector-by-sector correction again. We have a lot of near 52-week lows in Transports, Agriculture, Retail, Biotech, Materials, Financials, Homebuilders, Generic drugs, Energy and most semiconductors. Apple and Alphabet and Amazon—the three horsemen of the Nasdaq and S&P 500—are trading “heavy” as we called it on the trading desk back-in-the-day. Apple is the most exposed company to China trade tariffs and restrictions in the world--and as goes Apple, so goes the Nasdaq.

Now the bond proxies (REITS/Utilities/Consumer Staples) have sold off from profit taking and the Small Caps and Microcaps are leading the biggest winners and losers every day--NOT healthy. What’s working besides AMD and VEEV? Verizon and high-end apartment player Avalon Bay breaking out?

The market is more confused than a pimply teenager at a church mixer.

Have we seen the top in the 2019 market? Without a real trade agreement, it is very hard to not make that case unless the Fed brings the love with 2 rate cuts. But the $70 bond market is telling us the world economy is slowing—the $19 trillion Germany/France/Italy and the rest of Europe is in a basic recession—but as many have come to the conclusion “IF you can cure something by throwing money at it, and the ECB can, it will.”

But I think Professor Jeremy Siegel gets the market reality right when he says “the stock market sees about an 80% chance that the U.S. reaches a trade deal with China by late 2019, but those odds decline by the day. U.S. stocks were at all-time highs because there was an expectation in the market that Trump “has got to do a trade deal to get re-elected.” The stock market also believes that the stock market has to be higher than it is right now if Trump wants to get re-elected in 2020—and he knows it.

Is it different this time? Do the 25-year global supply chain and huge globalized multinational corporations plus an aligned highly stimulative and dovish Japan/EU/Fed Central Bank monetary policy defy the downside of the Trump/China game of corporate chicken and political machismo?

Please insert you best guess here._____________.

Our base case now is this:

There is no rabbit about to pulled out of the hat until China fires back and turns up the voltage with an economic nuclear bomb detonated in the US as powerful as the Huawei US semiconductor blacklist which means

Odds of China-US détente DO drop every week the tariff warfare increases and hostile tweets continue without new talks

The volatility VIX needs to once again hit >25-30 panic to get the “whoosh the panic bottom is in” and the bargain hunting going—the relatively low volatility is a head scratcher unless put option buyers are satisfied they have coverage past the June 20 G20 meeting

We are going to bet on an escalating (not deescalating) tussle until Dr. Tariff has launched ALL his economic missiles into the Chinese economy.

The Ultimate Case?

To me, the good news is that since the Trump administration has now said “no real structural reform, no deal,” we can presume that means a deal will require some structural change to their China neo-mercantilist business model. That kind of deal would logically make the market reaction more positive than just a basic truce that calls off the tariffs on both sides with some meaningless window dressing.

China has had its neo-mercantilist business model for 25 years and it likes it—a lot. It is proud of its hybrid capitalist/mercantilist model, so the question is “what significant part of their business model can they give up to take its stock market and slowing economy (lowest GDP growth since 2009) back to health? I don’t have a source inside the negotiations—but the IP protection provision/forced JV structure is the biggest outlier to the rest of the world. They have used it to help build an economic miracle over the last 25 years—isn’t it time to give up this underhanded and clearly illegal and unacceptable practice?

Conclusion:

The “trade agreement” process standoff means China has to give Trump some of red meat he wants or the tariffs explode which dips China into a virtual recession (their GDP “statistics” are highly manipulated) heading into their 70-year anniversary of the Chinese revolution.

Trump now has to get a deal that extracts some blood from China. If he settles for a photo-op settlement ala the North Korean “agreement” which is completely empty, the Dems go after him as a sell-out and weak and the farmers say “we got killed for this?” If he gets a real IP deal with real teeth in it, tech companies get a boost and he gets a major political talking point: “Look I stared down the Chinese and brought home the gold for America!” and the IP protection with real penalties is certainly a positive for American technology companies

The scariest part here is like I said a few updates ago: China is playing a very long game and now they cannot be seen as weak and folding too much to the American imperialists and damaging Chinese nationalist morale and losing Face.

Final conclusion—1) odds are extremely low this issue is settled at the June 20 G20 summit—that’s a pipe dream. President Trump, speaking during the state visit to Japan last weekend, said, "I think (Chinese officials) probably wish they made the deal that they had on the table before they tried to renegotiate it." Like I said, when the 75-page document came back for the final review and it was jammed with changes and deal point edits from the Chinese, the quick agreement play was DOA.

2) My 24 years in DC taught me that once you get past 4th of July and Congress is in recess, not much happens in DC of importance. We should plan for the worst (and we are with just a few risk stocks) but unless the Huawei blacklist gets extended after 90 days, we will take profits on Nvidia and wash them with a loss on this round of Xilinx as they just have too much exposure in China and Huawei.

Ironically—somebody better tell Xi that the only scale source for Huawei for their 5G FPGA chips is—Intel (via their Alteryx subsidiary) and Xilinx. Without them, the whole 5G rollout slows to a crawl (but it does put Ericson and to a less extent Nokia in a great 5G spot—working on that investment thesis now).

Reality: The Stock Market in the Short Term is a Sentiment Measurement Machine

All I really know for sure is this—human beings and bull/bear sentiment have not changed ever. We all still have the same DNA and emotional operating system and thus our behavior in times of stress and uncertainty are innately the same. Right now the innate human reaction in most global corporate board rooms is “Hey—let’s put the brakes on for the time being and see how this trade war plays out before we invest another $500+ million or $5 billion into new plants, equipment, staff, marketing etc.—this trade war could turn out to be more than a tactical skirmish IF each side escalates the tit-for-tat posturing tactics”.

That “sitting on our hands” behavior has now leaked into the economic cycle and a negative feedback loop and has pulled GDP growth down to 1% ish for Q2 and Q3 in the United States. Yes Virginia, corporate management capital budget risk/reward sentiment IS the marginal ingredient driving GDP expansion or contraction with a US economy 72% in services

Morgan Stanley economists have lowered their second-quarter U.S. GDP forecast to 0.6% from 1.0%. That comes after J.P. Morgan last week cut its own second-quarter outlook to 1% from 2.25%. “The April durable goods report was bad, particularly the details relating to capital goods orders and shipments. Coming on the heels of last week’s crummy April retail sales report, it suggests second quarter activity growth is sharply downshifting from the first quarter pace” their economists wrote.

The Wall Street Journal summarizes this pull back well.

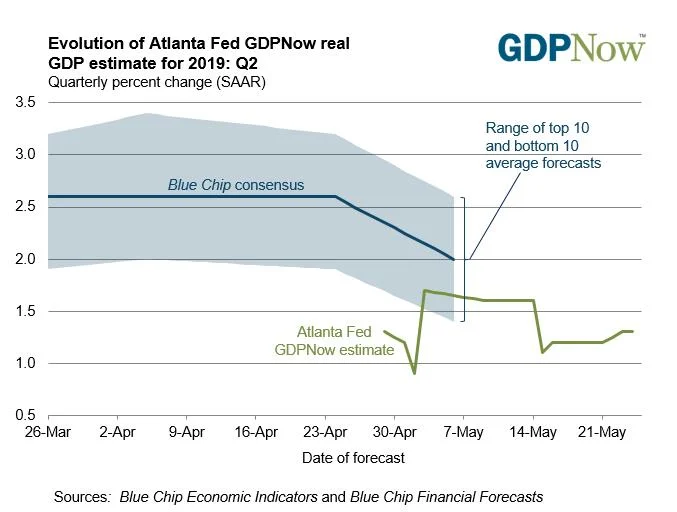

Well, guess what—our 45-piece economic data index has tanked as well. The Atlanta Fed’s GDPNow model estimate for real GDP growth (seasonally adjusted annual rate) in the second quarter of 2019 is 1.3 percent on May 24, up from 1.2 percent on May 16. After the U.S. Census Bureau's releases on new home sales and construction costs on Thursday, May 23, the nowcast of second-quarter real residential investment growth increased from -4.0 percent to -1.6 percent.

The New York Fed Nowcast stands a 1.4% which makes our Q2 forecast 1.35%

Our Transformity MacroMarket Index has fallen from 16.2 to 15.2 in the last 60 days.

Perhaps more worrisome is whether you love or despise Mr. Trump, we all can agree that anticipating his day-to-day behavior and tweets has become a losing parlor game. Most of Wall Street (and I) came to the base case assumption there would be a lot of Trumpian tweets and huffing and puffing in the run-up to the “final agreement just 2 weeks away” but that for deeply valued political reasons both sides would have to blink a bit and shake hands for the camera and walk away with an agreement.

The one thing for certain? The $22 trillion US bond market and the $40 billion EU and Japanese bond markets are not buying a quick happy ending. The key slice of the Treasuries yield curve is falling deeper into inversion (3-month/10-year) as the growing angst over trade friction means the Federal Reserve will cut interest rates by year-end.

The gap between 3-month and 10-year rates dipped Tuesday to negative 9.2 basis points. That’s the most negative since March when the curve first inverted since 2007. Gaps between most other sectors of the curve have narrowed as well. As you know, historically, an inverted curve has been a signal that a recession is looming. Renewed tensions in Europe did not help either and damped demand for riskier assets.

So let’s be real here folks—there is now irrefutable mounting evidence that the trade war is taking its toll on US companies and those around the world. In turn, almost every economic data point in the U.S., China, Asia and Europe are worsening.

The IHS Markit “flash” survey of U.S. manufacturers fell to a nine-and-a-half year low of 50.6 this month from 52.6 in April. Manufacturing conditions have been soft for months. Sentiment among manufacturers hit its lowest level in nine years—there is the “S” word again. What happened: The growth in new orders from both domestic customers and foreign buyers declined and firms “put the brakes on hiring," IHS said.

Even more ominous, Markit’s survey of U.S. service-oriented companies such as banks and retailers slipped to a 39-month low of 50.8 from 52.7. Service companies employ about four-fifths of all U.S. workers. Until recently they’ve been expanding rapidly. The sharp decline in the indexes this year suggests the U.S. economy will slow in the months ahead, especially if the dispute with China drags on.

The South Korean Won currency and export index aka the export canary in the world economic coal mine fell sharply last week into negative territory—not good.

The April reading on US durable goods/factory manufacturing dropped 2.1% across the board—but a majority of that drop was Boeing orders not delivered

Layoffs in the auto sector are climbing—Ford GM Chrysler

Copper prices are down 8.9% the past four weeks

US new homes sales dropped for the third month even with 2-year low mortgage rates.

The Dow Transports and small-cap Russell 2000 have underperformed the S&P 500 and Dow the past month

Utilities, consumer staples, and REITS are once again leading the markets and are seriously over-priced.

One of my favorite economic forecasters that I follow is Paul Ashworth at Capital Economics get the big picture right here “What surprises us is that, despite these signs of a rapid slowdown in U.S. economic growth and the renewed escalation in trade tensions, the S&P 500 has held up surprisingly well. If markets are pinning their hopes on a U.S.-China trade deal next month or on the Fed successfully saving the day, then they could be in for a rude awakening.”

Ashworth also believes incoming economic data point to a “sharp” slowdown.

The bottom line

Well on cue the Fed DID come in and save-the-day in early June with Chairman Powell doing his best “We acknowledge the trade war is taking a toll on GDP and if escalates increases odds of mild US recession.” and the pull back halted—for 5 days. But this dialogue suggests to me the market is one or two bad economic reports away from a sharp reversal as the dominant investment theses get blown up and replaced with a new base case: trench warfare till US/China trade settlement.

In general, Corporate America is NOT going to report bang-up second quarter results and now many are at >50% risk at cutting their 2019 outlooks. I encourage all investors to look up the earnings calls from retailers like Target, Walmart, Kohl’s, Gap, Macy’s and Best Buy to get a sense of the real profits the trade war is stealing or the major export manufacturers like Deere, Caterpillar and Boeing cutting end demand

In short, the Q2 slump and second half 1% ish GDP growth has to get priced into stocks. Plus Mr. Trump appears to be trigger happy to slap 25% tariffs on the remaining $325 billion worth of Chinese goods that have not already been taxed. The Chinese retaliation will be to impose export tariffs on more American goods.

But the REAL Chinese retaliation is to

a) they let the yuan rise/devalue to >7.3 per dollar

b) flood their economy with more liquidity

c) Watch the US stock market crash as the $dollar explodes in value and kills exports

THAT IS the only tit-for-tat that matches Trumpist tariffs. It would cause a flight of yuan out of China--but it is the only nuclear bomb China has to match 25% tariffs on $600 billion of exports and permanent disruption of Chinese supply chain providers.

China has sent strong signals that it won't back down, with state media saying the United States' trade deal demands threaten the country's "core interests," a term usually reserved for territorial disputes such as Taiwan.

It is not time yet to be contrarian. When we see the VIX chart look like explode over 30+ on big volume, it's time to be brave.

We will send the update on the China rare earth situation ASAP--but the short version is just like 2010 in the last shut down by China--its not the real threat. The real threat is for China to turn on the monetary spigots again and allow the yuan to rise to over 7 yuan for every dollar--THAT is how you deliver a financial nuclear bomb into America.

Have a great weekend...cash is gorgeous.