Announcing TR Pro Investor's 2025 $5 Trillion EV Transformation Portfolio

Dear Subscriber,

We teased you last week with this note saying "we are finalizing our 2025 portfolio with a fantastic opportunity to buy a junior North American graphite mining and processing company in a few years for .18 cents or better with a $2.25 target price in late 2023.

That stock is Quebec-based Lomiko Metals, Inc. ticker LMRMF. We have spent many months in a deep dive into researching and building a 2025 Battery Electric Vehicle Transformation portfolio.

Action to Take: BUY LMRMF at 2X Normal TR Pro Allocation at .18-.20 or better

Target Late 2023: $2.25 with mining permit and mining operations commencement (or higher with buyout)

The Short Version of the EV Grade Graphite Demand Explosion In the Race to BEV Mobility Dominance

We are launching our new 2025 Ultra Growth portfolio today consisting of the technologies and materials enabling the $5 trillion 2020-2025 transformation to battery electronic vehicles ("BEV")/ green power grid storage and green hydrogen that have 300%-500%+ upside over the next 4 years.

And sure enough, this week ALL the stars have aligned to tell us the rate of the $5 trillion global transformations to electric battery-powered vehicles ("EV Mobility" for short) has just hit WARP SPEED.

In addition to the Biden Administration's upcoming $4 trillion green energy infrastructure spending and development plan to get the United States off carbon-based energy by 2045 (the first leg of which is a $400 billion EV infrastructure bill for charging stations etc. ) will pass the Congress with another "reconciliation" bill that requires just 50 Senators to vote yes and VP the tie-break), Europe and China committed this week to an even faster decarbonized "mobility" system by 2035 and 2040.

Then the provinces of Quebec and Ontario announced yesterday they have committed $100+ million to make Quebec and Northern Ontario (big auto manufacturing and assembly hub) a BEV Development Zone. Quebec has the lithium, nickel and most important high-grade graphite resources and Ontario has the BEV assembly manufacturing resources. The investment will take the form of a loan to Lion Electric, a Saint-Jérôme-based company that makes electric trucks and school buses. Roughly $30 million will be forgivable if the company meets certain conditions, including keeping jobs in Quebec. Lion Electric plans to use the funding to build a new $185-million factory in Saint-Jérôme, north of Montreal, where it will assemble battery packs for its vehicles. That would allow it to cut unit costs and potentially capitalize on the growing market for greener transportation options. "When we talk about an economic recovery that's good for workers, for families, and for the environment, this is exactly the kind of project we mean," Premier Trudeau said at a news conference in Montreal.

KEY POINT: Where do the graphite and lithium and nickel come from to make millions of EV battery packs?

From Quebec of course!

Key Point: The project also aligns with the Legault government's plan to create a world-class supply chain within Quebec ofEV raw materials that are able to feed the electric vehicle industry. At Monday's announcement, Economy Minister Pierre Fitzgibbon spoke at length about the province's deep deposits of lithium, nickel and graphite — key components in electric vehicle batteries — as well as its supply of low-emission hydro-electricity.

"If we play our cards right, we could become world leaders in this market of the future," Fitzgibbon said.

Bingo!

Then the VW Shock and Awe BEV 2030 Domination Plan

The ginormous $40 billion VW "Shock and Awe" BEV Plan 2025 plan was announced over the last 2 days. VW and its worldwide ICE ("internal combustion engine") vehicle empire are now ALL IN on its BEV future with 70 BEV MODELS on tap for introduction over the next 24-36 months. VW just placed a $14 BILLION order for lithium-ion ("LI") batteries and with LI battery partner so they are building 6 "gigafactories" (gig is one billion) that can all produce one billion gigawatts of EV power per plant per YEAR!

VW's "all in" move has now kicked the BEV Mobility transformation into high gear and now the table stakes for the other legacy players have multiplied by 2X to $40 billion. There are going to be losers of course in the BEV Mobility race just like the ICE auto industry where we had 200+ automobile manufacturers in the US starting in the 20's and finally wound up with the Big 3 GM Ford and Chrysler.

But VW is now assuredly going to be one of the BEV winners and, with $80 billion market cap/10 p/e vs. $680 billion Tesla at an 800 p/e, we are going to add VW ADRs to our 2025 BEV Mobility portfolio on pull backs. GM and Toyota are fully committed to BEV mobility as well, and each has an ambitious EV rollout plan 2021-2023 as well that includes manufacturing their own LI-ion battery packs.

If you want to get a quick education in the world mobility market in 2025, take a moment AFTER you buy a good chunk of LMRMF for your 2025 portfolio to read my old neighbor in Bethesda, Maryland Steve Levine now at Medium.com whose work over the last 12 months is the best EV mobility journalist going. Here is a link to his Mobilist blog.

So what the heck does all the above have to do with high-grade graphite mining and processing?

Answer: NONE OF THE ABOVE happens without 10X more MASSIVE amounts of high-grade EV quality graphite used to build the EV battery ANODES.

Most human beings have no idea how an EV battery works (or any battery for that matter). But the name "lithium-ion" makes people assume an EV lithium-ion battery is mostly lithium--eh--it is not. There is (on average) 15,000% or 15X more GRAPHITE in a LI battery than lithium. There is 10x more nickel in an EV battery--that is why Elon Musk famously says "We should call our batteries nickel graphite batteries since that is actually what they are made of!"

All the above is how we get to Lomiko Metals LMRMF with a .18 cent buy under and $2.25 target in late 2023. LMRMF is a Quebec-based flake graphite miner that is simply in the right place, right time, right flake graphite space that by definition all the analysts in the space forecast demand from lithium-ion BEV's grows 500-700% from today to five years from now.

Silicon graphite composites are the anode materials for Li-ion batteries with small amounts of silicon and different binders enhancing the energy density of the graphite anode. LI batteries have both an anode and cathode. The Anode is the negative or reducing electrode that releases electrons to the EV motor via the battery's electrochemical reaction. The Cathode is the positive or oxidizing electrode that acquires electrons while being charged from an external circuit and is reduced during the electrochemical reaction.

Key Investment Point: The way to make the most $$$ in the flake graphite miners ( or any EV related metal or mineral in fact) is to buy the "junior" player before their resource numbers (size of deposits and life span of deposits) are validated by a "PEA" or Preliminary Economic Assessment.

It's the PEA from an independent licensed resource economics professional team that states the economics of a specific mineral or metal play. I have seen the resource work so far for just two of 12 graphite rich regions in the Lomiko graphite mine (LMRMF CEO long time friend) and lets' just say that given the projections by ALL the BEV companies and analysts that the demand for natural graphite (versus synthetic graphite that comes from coal or coke--NOT GREEN!), we expect a 75-125% increase in the resource estimate for just the 2 initial plays--there are 10 more of similar size left to mine!

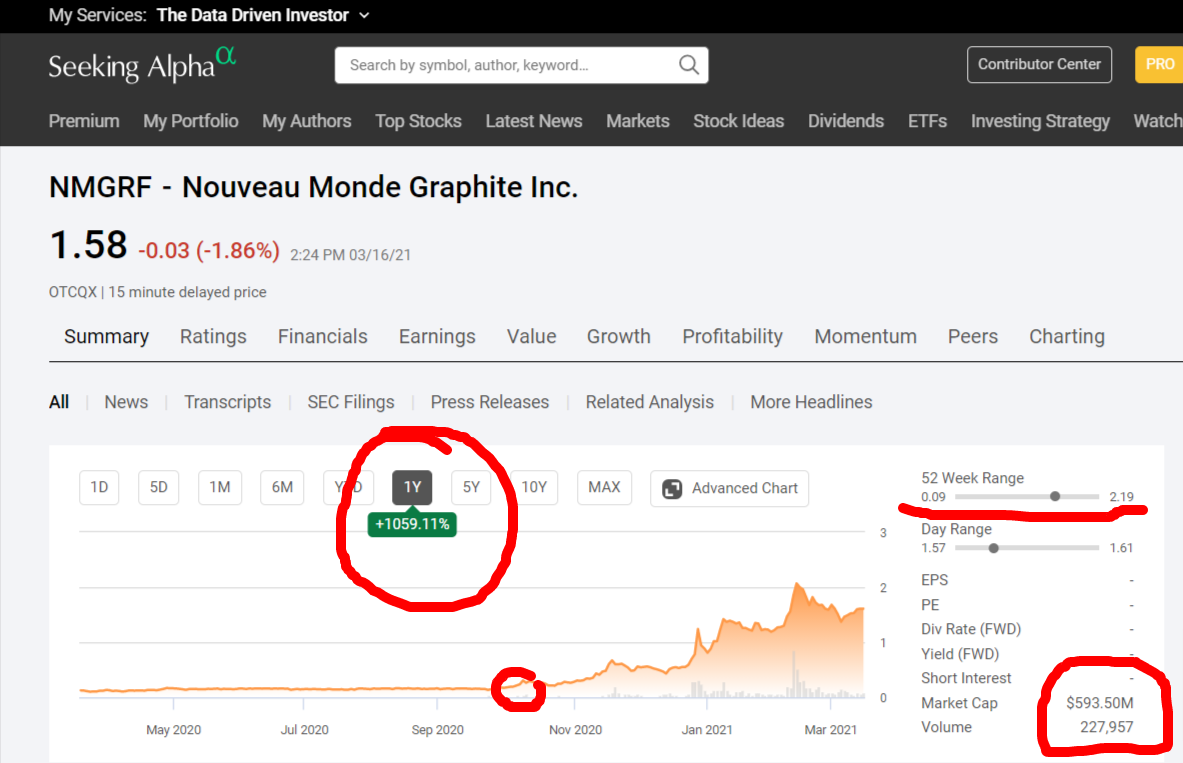

The Other Key Point: We have a very valid and recent Valuation Comp for Lomiko--it's Nouveau Monde's (NMGRF) graphite project nearby in Quebec that has recently received its mining permit. NMGRF is only up 1000% in the last six months. They are in the same geological region, have the same quality flake graphite reserves as Lomiko which is 200km southwest of Nouveau Monde's Matawinie mines.

Here is the NMGRF chart as they went on a 1,000% run from PEA to mining permit over the last 12 months...mmmmm!

Get it now? We missed a ten-bagger NMGRF--now we have an even bigger opportunity with LMRMF--and you KNOW that the success of NMGRF stock is going to bring a LOT of attention to "OK--who is the NEXT Nouveau Monde???

But Wait--There's More! Here is the Secret Sauce for Lomiko That is So Killer!

The big dog in the flake graphite space in Quebec WAS a $4 billion market cap carbon and graphite miner multinational Imersys. The secret sauce for Lomiko is that the Imersys graphite mine is just 53km from Lomiko's graphite and IMERSYS's mine is going to CLOSE in 2022--they have mined out ALL THEIR flake graphite reserves!!!

Lomiko CEO Paul Gill tells TR that "Our flake graphite is virtually identical grade to the Imersys graphite. That means we can sell OUR graphite to Imersys to upgrade and process (called an "offtake" agreement) and the BEV end users will be happy since the graphite is virtually identical grade." In addition, the miners and processors currently at the Imersys mine will be available for hire at the Lomiko graphite mine--we get an instant highly skilled and 20-year experienced workforce!

What Mr. Gill did NOT say is what I think is obvious: WHEN Lomiko gets its mining permit ala Noveau Monde, $4 billion market cap Imersys in my opinion would be CRAZY not to BUY Lomiko outright and test the 10 remaining OTHER graphite reserves on the Lomiko property and BUY LOMIKO outright

OK Here is the Timeline to a $2.50 LNRMF Stock Price--10X Higher Annual Demand for Flake Graphite in 2030

The fair present value today of LMRMF proven and unproven flake graphite reserves are .32-.35 per share.

Next, the LMRMF PEA report out is out in September...and based on the 2016 resource estimate, Lomiko is a .75-.85 stock by year-end with a proven 25 year+ mining operation or a $4X-5X winner but not done yet.

NOW--based on the new consensus of 40 million BEVs by 2030 (which is also the time range that higher density solid-state EV batteries have become commercialized and scaled and reduce graphite demand) and since it takes 50 kilograms of flake graphite required PER VEHICLE for their battery packs, the leading graphite demand analysts Benchmark Intelligence estimates that the demand for NATURAL graphite (i.e, green not carbon synthetic) for EV batteries will increase to 2.6 MILLION TONS per year over the next decade.

Today graphite demand for batteries is 0.2 tons.

The BIG Question: Where is ALL THAT 10X more flake graphite going to come from????

Lomiko has secured $40 million in project finance debt from an NYC mining finance company (i.e., no dilution) from an outside party at very generous terms (4% interest paid back as mining revs ramp and warrants.)

As mentioned above, the analog for the price increase/value increase of Lomiko Metals in Quebec is Noveau Monde's property that just received a mining permit. NOU market cap today is $590M... LMRMF is $25M.

As I always say, "do the math!"

Advice: Don't wait too long to build a LMRMF position--we are using this amazing 10-bagger opportunity in our upcoming TR PRO marketing campaigns...YOU are not the only one getting our proprietary research OK?

PS: Here is the short version of Steve Levines latest article on the BEV Mobility Wars.

Boring old batteries have rarely had it so good. A good two centuries after their invention, they are sought-after with the same fraught urgency of the prospectors who hunted oil in the middle-late tailfin decades of the last century. The latest to make this bald determination plain is Volkswagen, which is throwing everything at an electric coming-out party meant to demonstrate its tech-on-wheels bona fides.

Yesterday, the German company held an almost two-hour international webcast to tout its quest to master battery parts rarely earning such attention, such as high-manganese cathodes and lithium-metal anodes. Its executives summoned a global press conference at 4 a.m. Eastern today in case the media had follow-up questions. One set of impressed folks was Wall Street, who yesterday bid up VW’s share price by more than 7%, to heights not seen since before Dieselgate, the shameful chapter of smog-device cheating that the company hopes will now finally be consigned to history.

As part of the multiday VW show, Dustin Krause, director of e-mobility for VW North America, passed not far from my home in the Washington, D.C. suburbs on Saturday. He was on an 18-day, cross-country PR journey in an ID.4, the company’s just-released electric crossover SUV. My elder daughter and I went to take a look.

“Fast charging” is a tricky word when it comes out of the mouths of people promoting batteries or EVs, but in this case, VW really does mean pretty rapid. That morning, Krause said, he had pushed 200 miles of charge into the battery in just a half-hour. He said you can do that every time with no serious degradation to the battery, which comes with an eight-year, 100,000-mile guarantee. “If you decide to do the same trip we are taking,” he told me, “it would cost you nothing.”

As part of its penance for Dieselgate, VW was forced to spend $2 billion on EV charging infrastructure. The result is superlatively advantageous for Volkswagen. It is Electrify America, currently comprised of some 550 fast-charging stations across the United States. VW is adding 3,500 more fast chargers to the network this year, and more still after that, all with the conviction that ordinary motorists won’t buy an EV if they don’t see charging possibilities everywhere and know they can get in and out quickly.

Here is the thing: The wisdom of almost every automobile and battery expert out there revolves around two axioms of the new EV age — that fast charging is largely unnecessary and only of use for the marginal occasion when one is traveling long distance; and that, when public charging is built, it will be almost exclusively at destinations like hotels, stores, and restaurants. With Electrify America, however, VW has declared war on both dubious assertions.

It’s doing the same everywhere. At “Power Day,” a virtual VW event yesterday in which the company described a massive rollout of charging infrastructure, company executives detailed plans to spend $477 million by 2025 on some 18,000 fast chargers in Europe, in addition to about 17,000 in China. “Charging will be as easy as refueling,” VW CEO Herbert Diess told reporters this morning in the webcast from Germany.

Over the last several months, Elon Musk, executives of GM, and the lithium-metal juggernaut QuantumScape have held gauzy events to flaunt their claims to current or future battery supremacy. Tesla has the earliest and largest network of fast chargers, and GM is building one with partner EVgo, but VW now appears to be the most aggressive. In the events yesterday and today, company executives unveiled a shock-and-awe roadmap to electric dominance.

The charging network was core, but VW also announced plans to build six battery gigafactories by 2030, for starters placing a $14 billion, 10-year battery order with Northvolt, a European foundry in which VW is a 20% owner. It announced integration with partners in the oil, electric, software, and other industries. Some of the battery and EV promises were deeply aspirational and unproven, such as 12-minute fast-charging; others were naked thefts of the aspirations of other people, like Musk. Yet in depth, scale, and sheer volume of daring bets, VW may be unsurpassed. Combined, the pledges were a message: If you are not Tesla — far ahead of the pack already — this is a roadmap to compete.

A core factor in VW’s electrification roadmap is the creation of what it called a “unified cell,” a single battery format and formulation that by 2030 would be common to about 80% of company EVs. The scale of VW production, brought to bear on that unified design, would have a powerful impact on cost, executives said. The cost of batteries for super-mini automobiles for the Indian, Chinese, and other Asian markets would be reduced by half. The cost of batteries for higher priced vehicles but still mainstream, mass-market vehicles would drop by around 30%.

Since batteries are by far the most expensive component in an EV, that would seriously lower the sticker price of these vehicles, thus bringing them into the buying range of the mass market.

This unified cell will be introduced at the end of 2024, but VW did not spell out what would be inside that battery. For the superminis, it described plans to introduce a relatively low-energy formulation called lithium-iron-phosphate, or LFP. And the end goal would be a battery featuring a lithium-metal anode, for which QuantumScape is VW’s primary partner. Currently, QuantumScape is very early in scaling up, with a four-layer cell, compared with the eventual 100 layers that are ultimately required for the battery. The hope is that it will produce a commercial version for use in high-end VWs by 2024.

James Firth, head of energy storage for BloombergNEF, said he expects a slow scale-up for QuantumScape and volume production only in 2030 or after.

So if the unified cell from 2024 through the end of the decade isn’t LFP, and it’s not lithium-metal, what is the thing that is going to start bringing down VW’s costs?

Another formulation that VW executives mentioned is a high-manganese cathode with nickel. Conceptually, experts like such a battery for its extremely low cost. Sam Jaffe, managing director of Cairn Research, a battery consultancy, told me that he expects German company BASF, for instance, to introduce a cathode made of 70% manganese next year. Yet, a BASF spokeswoman said the company is working on the technology but has no set timeline for commercialization. And VW spokesman Stefan Ernst told me, “high manganese is in development, and at this time, we won’t comment on market launch.”

Which leaves the current workhorse NMC, the chemistry in nearly every EV battery on the planet. VW mentioned using silicon in its anodes, and in fact, it already does in its Porsche Taycan and Audi e-tron. But that won’t deliver the announced cost savings. Therefore, as of now, VW is probably stuck with NMC on one side of the battery, silicon graphite on the other, and no clear immediate roadmap to the kind of cost reduction it is discussing—at least nothing greater than anyone else can produce.

All in all, battery scientists familiar with all the public battery events saw striking similarities between what VW announced and Tesla’s Battery Day. Shashank Sripad, a PhD candidate at Carnegie Mellon, tweeted that Musk was talking about a total 56% drop in battery costs from his various plans; VW is forecasting 50%. From the design of the cell, the cost reduction was 14% and 15%, respectively, from the manufacturing process, 18% versus 10%, and so on. Basically, it looked like VW was taking notes on Battery Day and embraced the Tesla ideas it liked.

Although it is almost the very beginning of the predicted new electric vehicle age, VW, GM, Tesla, Hyundai, and Chinese companies like Nio are already grabbing the commanding heights. After this, unless you have a blockbuster invention or a lot of cash, there may be little more than niches to fill — lots of niches, but niches still.